Fed’s headed for a showdown with the bond market

As the FOMC meets for a 2nd day, they will likely take comfort in what has occurred since their last meeting where they took the daring...

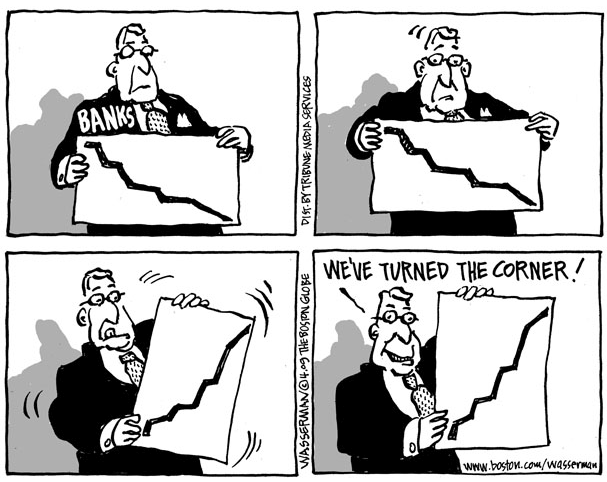

Ugly Process: Rationalizing Insolvent Banks Existence

Of the many issues that arise via the banking bailouts we have seen, perhaps the most pernicious is how corrosive the process becomes. It...

Of the many issues that arise via the banking bailouts we have seen, perhaps the most pernicious is how corrosive the process becomes. It...

Banks and Economic Data Wrestle to a Draw

Good Evening: Multiple crosscurrents prevented stocks from making much headway in either direction today, with the major averages...

The Big Picture Conference: Capitalism After the Crash

I mentioned a few weeks ago we were hosting a conference in NYC on June 3 2009. The conference is coming together nicely, with some...

inflation/bonds

While commodity prices have sold off the past 2 days due to concerns with the impact that swine flu will have on global growth, the...

Afternoon Reading

Today’s readings: INVESTING & TRADING • Estimates of economic costs of a flu pandemic (Telegraph) The World Bank estimated in...

The Next Great Bubble?

Vitaliy N. Katsenelson, CFA, is director of research at Investment Management Associates in Denver, Colo., and he teaches a graduate...

I am a “prophet of doom”

heh heh: Meet the Cassandras, 14 economists, bloggers, politicians and businesspeople of all political stripes who have become the most...