Budget Deficit Blowback

One of the striking things about about the deficit crisis that seems to loom over the United States is the probability that it will force...

Dennis Gartman of the Gartman Letter appears to have a rather vocal critic in Fabrice Taylor at The Globe and Mail, this item appearing...

Dennis Gartman of the Gartman Letter appears to have a rather vocal critic in Fabrice Taylor at The Globe and Mail, this item appearing...

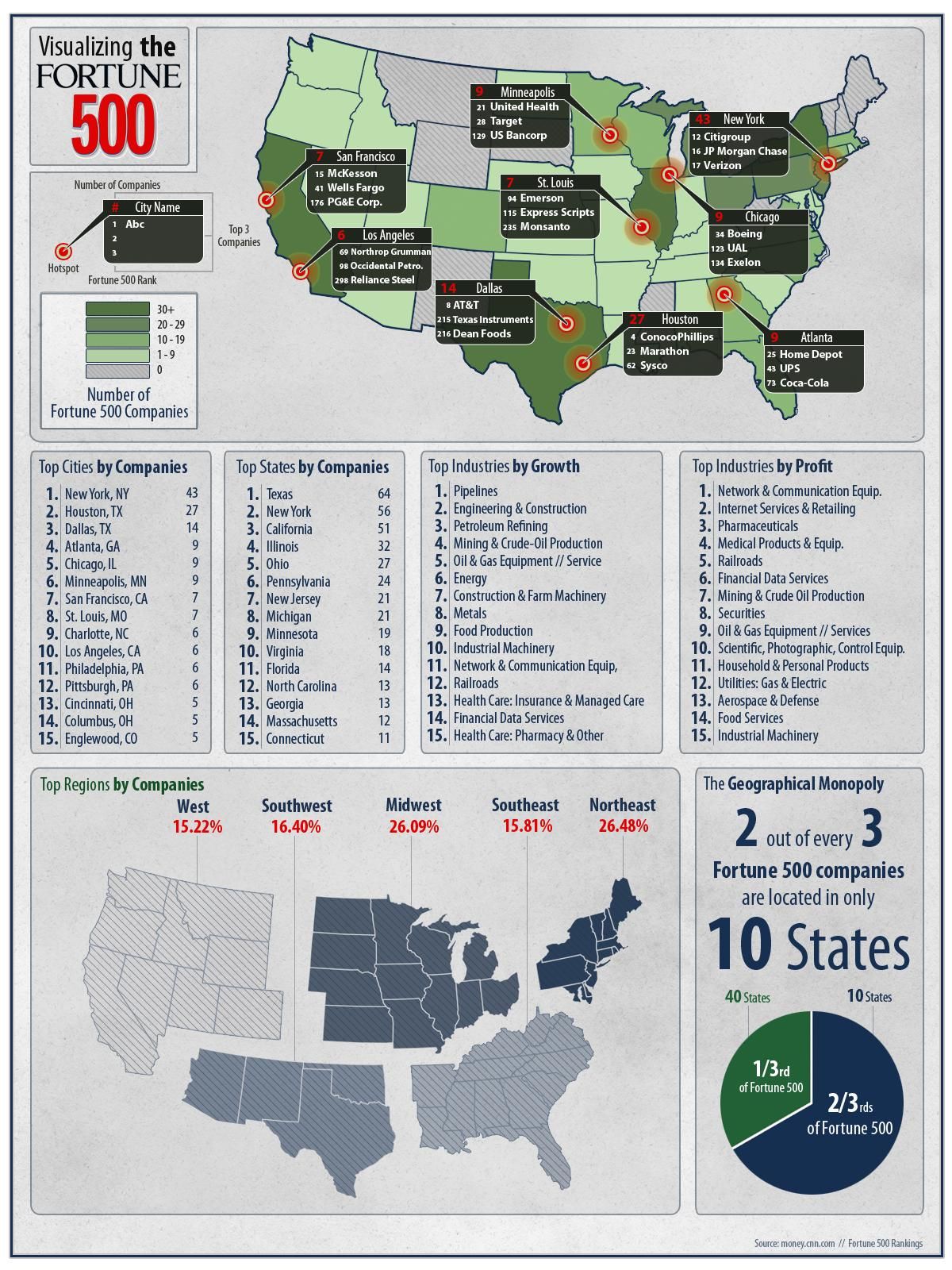

Via Focus.com, we have this interesting map of where the Fortune 500 are located: click for ginormous map

Via Focus.com, we have this interesting map of where the Fortune 500 are located: click for ginormous map

Well, apparently there is at least one thing that former Vice President Dick Cheney and Nobel Prize winning economist (and unofficial...

Well, apparently there is at least one thing that former Vice President Dick Cheney and Nobel Prize winning economist (and unofficial...

Since we have spilled so many pixels on retail and consumer spending, let’s look at some charts as to what and how much Americans...

Since we have spilled so many pixels on retail and consumer spending, let’s look at some charts as to what and how much Americans...

Get subscriber-only insights and news delivered by Barry every two weeks.