The Place Where Reform Goes to Die

One of the best things I have ever read on Huff Po — The Cash Committee: How Wall Street Wins On The Hill — explains how...

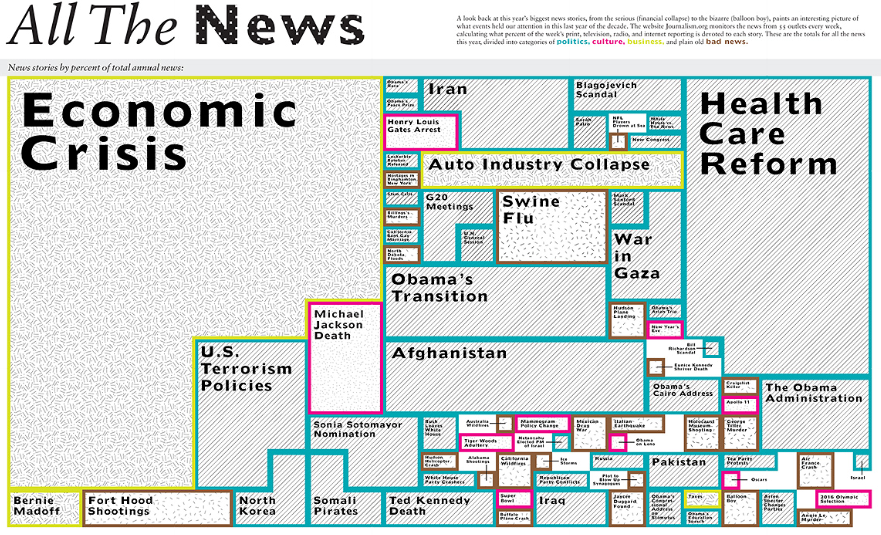

In lieu of our usual lunch time chart, let’s have a go at this cool infographic, via Good, showing the biggest news stories of the...

In lieu of our usual lunch time chart, let’s have a go at this cool infographic, via Good, showing the biggest news stories of the...

~~~ HAPPY HOLIDAYS and HAPPY AND HEALTHY NEW YEAR! ECONOMY As first forecast last March, the U.S. economy was going to experience a...

~~~ HAPPY HOLIDAYS and HAPPY AND HEALTHY NEW YEAR! ECONOMY As first forecast last March, the U.S. economy was going to experience a...

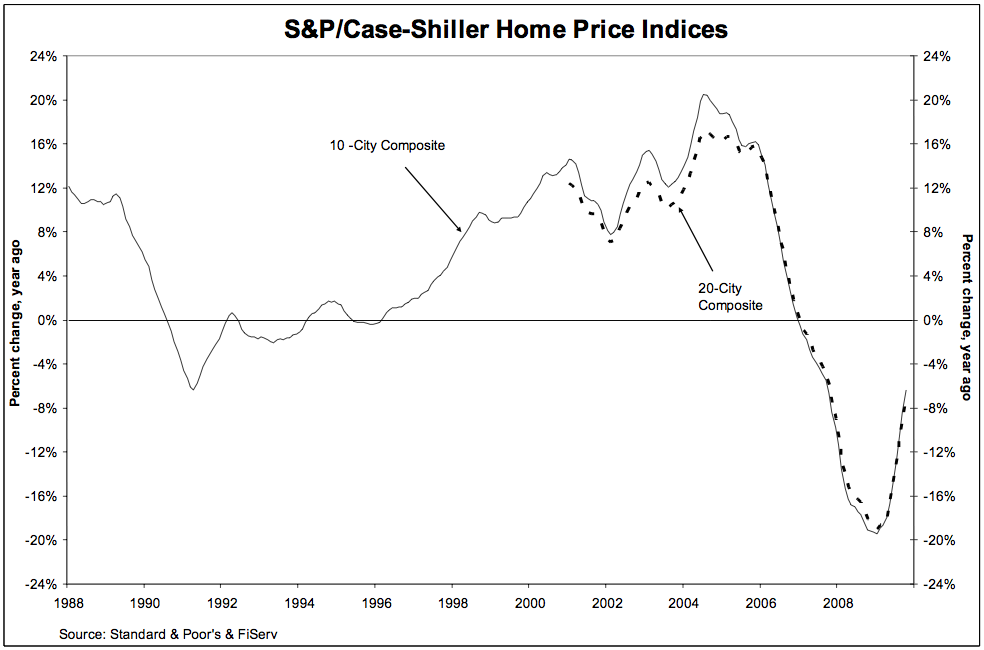

The latest data from Case Shiller, covering the October 2009 period, shows an ongoing improvement in price data. This was the 9th...

The latest data from Case Shiller, covering the October 2009 period, shows an ongoing improvement in price data. This was the 9th...

The post-holiday mark downs continue: I spotted my camera — Panasonic Lumix DMC-ZS3 10.1 MP Digital Camera with 12x Wide Angle MEGA...

The post-holiday mark downs continue: I spotted my camera — Panasonic Lumix DMC-ZS3 10.1 MP Digital Camera with 12x Wide Angle MEGA...

Get subscriber-only insights and news delivered by Barry every two weeks.