How cool is this, from Gonglue Jiang, a desing student at Zhejiang University: > via Design Fetish

How cool is this, from Gonglue Jiang, a desing student at Zhejiang University: > via Design Fetish

Read More

These few stories caught my eye today: • Obama: Drill Baby Drill (NYT) • The Lone Star Secret: How Texas avoided the worst of the...

Read More

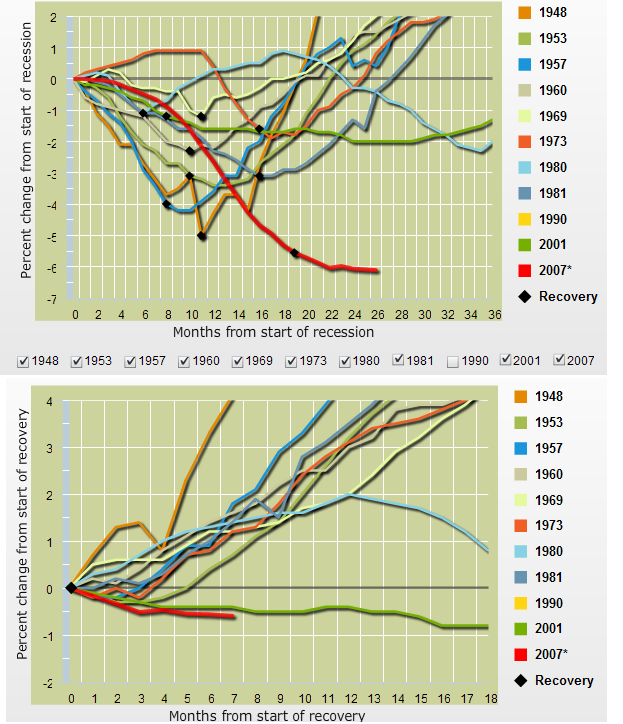

If you found the prior post on Employment too cheerful, well, have a gander at these charts, courtesy of The Federal Reserve Bank of...

If you found the prior post on Employment too cheerful, well, have a gander at these charts, courtesy of The Federal Reserve Bank of...

Read More

To add more fodder to the inflation/deflation debate, the Journal of Commerce Industrial Commodity Index of 18 industrial materials is...

Read More

Matt Trivisonno shares with us some of the research he does at Daily Jobs Update regarding payroll withholding taxes. He notes that in...

Matt Trivisonno shares with us some of the research he does at Daily Jobs Update regarding payroll withholding taxes. He notes that in...

Read More

Greece still is getting no respect. While global bond markets are rallying in response to the weaker than expected ADP report and the...

Read More

The Mar Chicago PMI manufacturing index was 58.8, about 2 pts below estimates and down from 62.6 in Feb which was the highest since April...

Read More

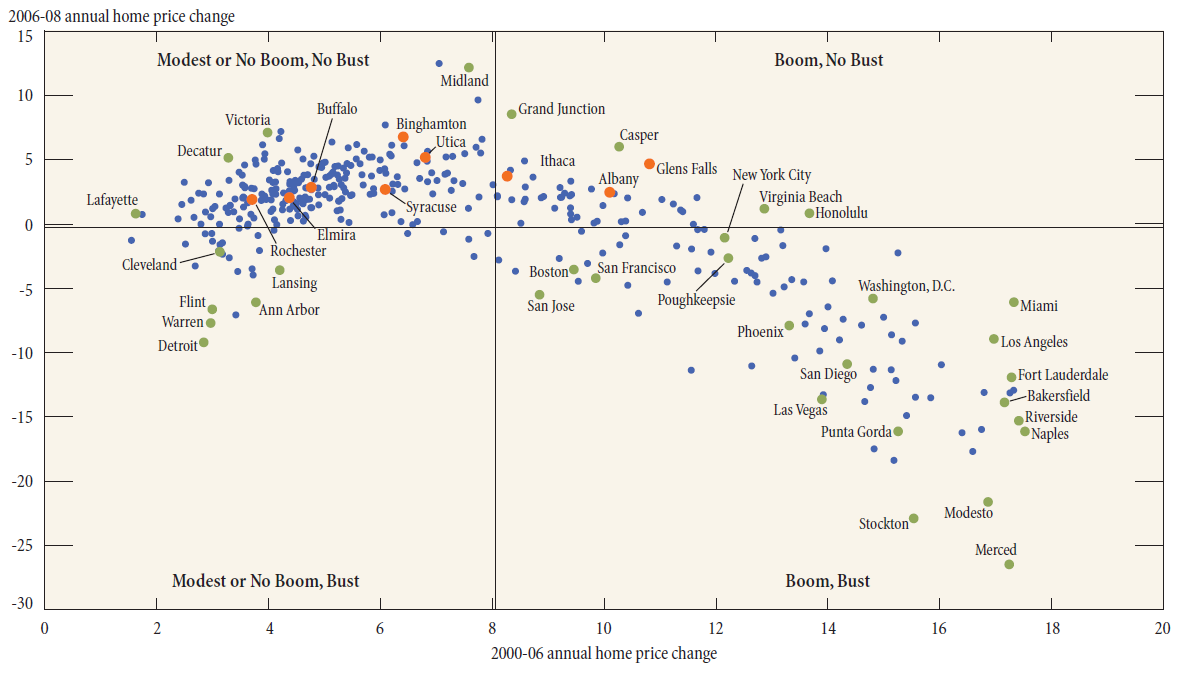

The NY Fed has a curious research piece out, looking at areas of Upstate New York that were “insulated” from housing price...

The NY Fed has a curious research piece out, looking at areas of Upstate New York that were “insulated” from housing price...

Read More

Be sure to check out the excellent overview of the present situation from Damien Cleusix in the Think Tank: Global Tactical Asset...

Read More