Confidence bounces, labor market answers improve, but where the...

Conference Board Consumer Confidence was 52.5, 1.5 pts higher than expected and up from 46.4 in Feb which plummeted 10 pts from Jan. The...

A design student’s eco-friendly and edgy reworking of the Coke bottle. This is only the first quarter of it — the full piece...

A design student’s eco-friendly and edgy reworking of the Coke bottle. This is only the first quarter of it — the full piece...

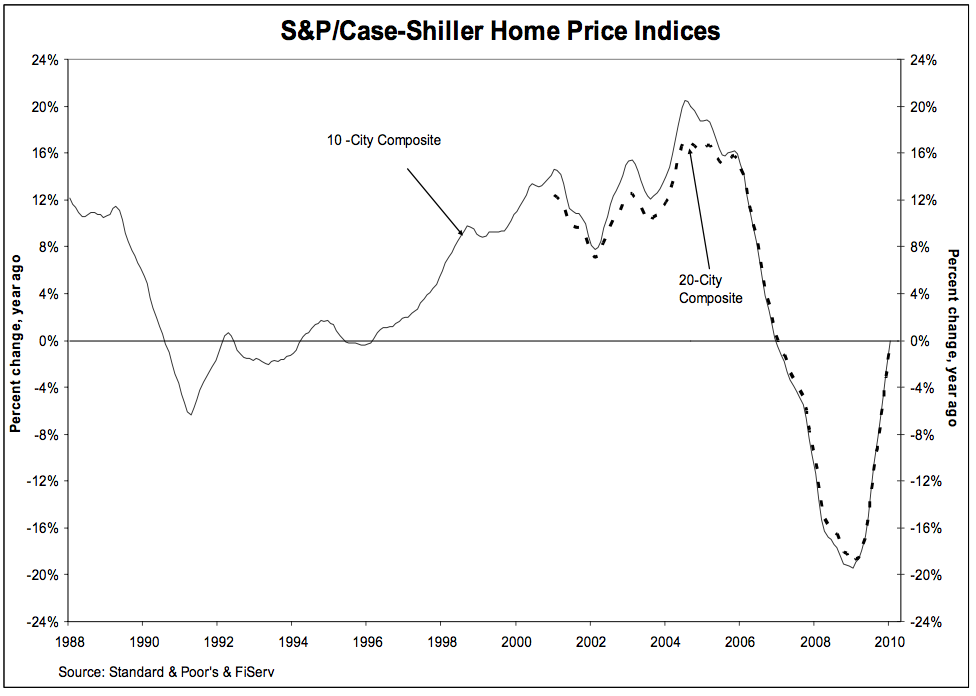

Case Shiller data through January 2010 was down only 0.7% versus January 2009. The report was mixed. There were improvements in the...

Case Shiller data through January 2010 was down only 0.7% versus January 2009. The report was mixed. There were improvements in the...

Get subscriber-only insights and news delivered by Barry every two weeks.