Plosser says no mas for now

Non voting Fed member Charles Plosser in a speech on the economy is saying, “Because I see little gain at this point, and some...

Doug gives the Themis Boys some props, and he does the same to BATS. Guest Post: The Story of Canada Bill Jones by Doug Clark of BMO The...

Doug gives the Themis Boys some props, and he does the same to BATS. Guest Post: The Story of Canada Bill Jones by Doug Clark of BMO The...

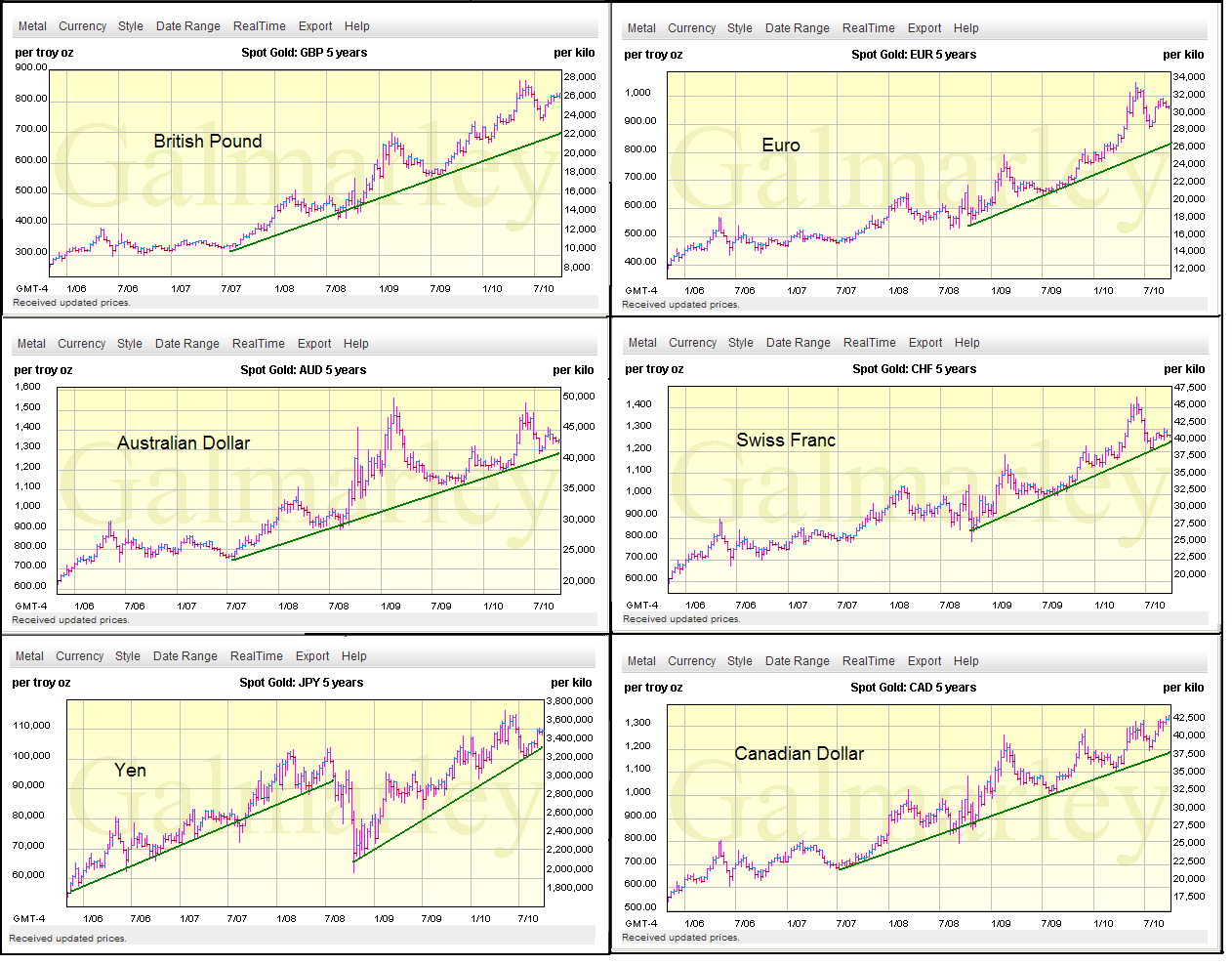

Not so much, according to Jesse’s Café Américain: “But the US dollar is not alone, not the only fiat currency in a bit of a...

Not so much, according to Jesse’s Café Américain: “But the US dollar is not alone, not the only fiat currency in a bit of a...

If you are interested in owning the fastest production car Maserati makes, than its the MC Stradale: > > via Classic Driver

If you are interested in owning the fastest production car Maserati makes, than its the MC Stradale: > > via Classic Driver

Everywhere I turn is another article about Quantitative Easing Part 2. Will they or won’t they? My question last week was will it make...

Everywhere I turn is another article about Quantitative Easing Part 2. Will they or won’t they? My question last week was will it make...

Get subscriber-only insights and news delivered by Barry every two weeks.