Shiller’s cyclically adjusted price-earnings ratio

click for ginormous chart

Source: Bloomberg

Robert J. Shiller, a co-winner of this year’s Nobel Prize in Economic Sciences says US stocks are expensive. They are the most expensive relative to earnings they have been in more than five years — since the lows follwoing the great collapse of 2007-09.

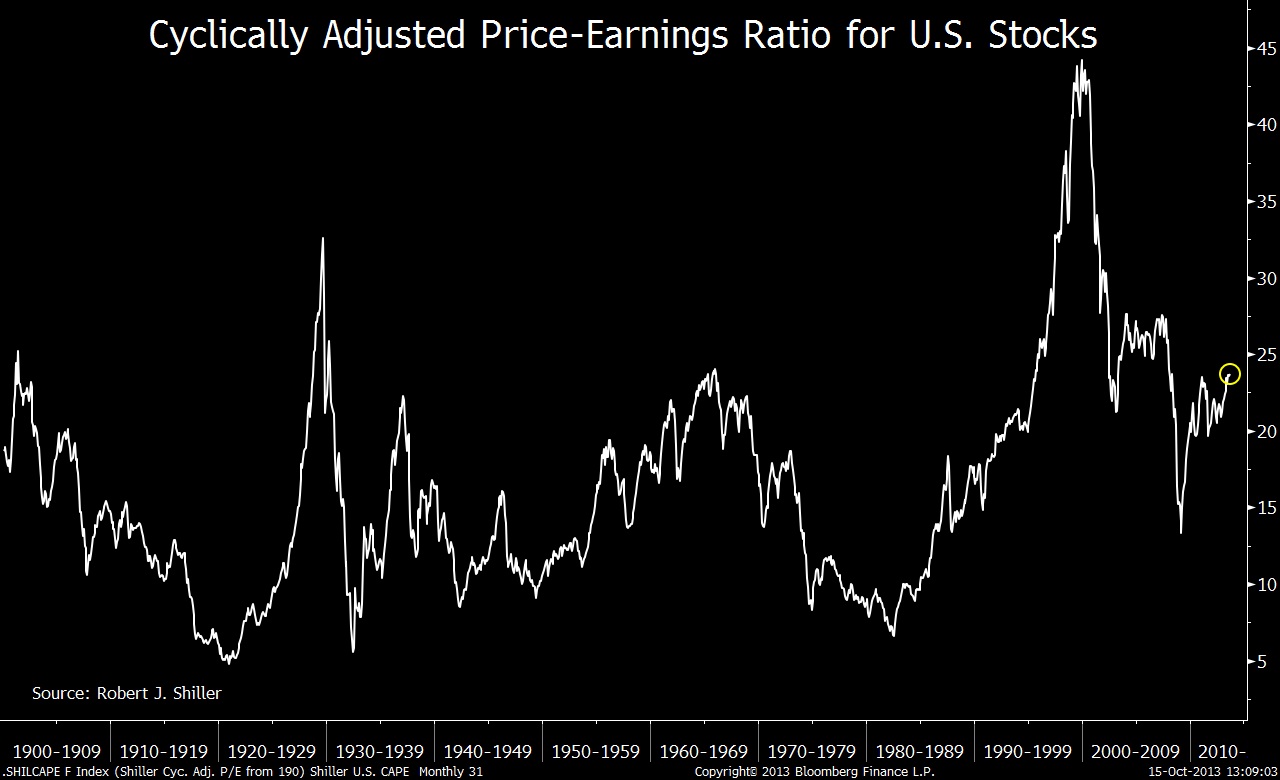

Shiller’s CAPE ratio — the cyclically adjusted price-earnings ratio — compares the Standard & Poor’s 500 Index with companies’ average profits over the prior decade. The ratio ended last month at 23.7, the highest since January 2008, according to data available from his website.

Bloomberg notes that “the September ratio was lower than a peak of 27.5 in May 2007 — and even further below a record of 44.2, set in December 1999.” Date for Shiller’s price-earnings figures go all the way back to 1881 (above chart 1900 – present).

Shiller made several other comments on equities:

“The stock market is rather highly priced. I worry that it might correct down.”

“I don’t think one should view it with alarm.”

“One could well — and probably should, in a diversified portfolio — invest in stocks.”

A far cry from his prior warnings of dot com stocks in 1999 and housing in 2006.

The CAPE ratio was developed by Shiller and Harvard University professor, John Y. Campbell.

Source:

Chart of the Day: Shiller Views U.S. Stocks as ‘Highly Priced’:

David Wilson

Bloomberg 2013-10-15

What's been said:

Discussions found on the web: