If They Will Lend, Someone Will Spend (on Something)

Paul Kasriel

March 17, 2014

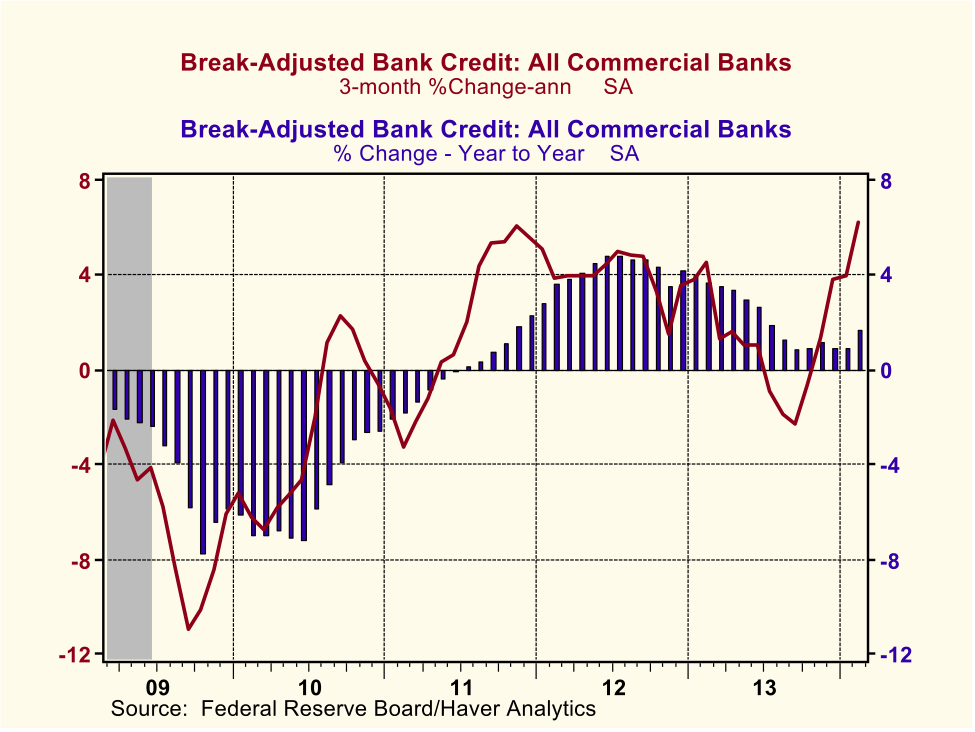

Upon awakening from my winter hibernation way up here in beautiful northeastern Wisconsin, I have noticed that bank asset managers have been anything but hibernating. Rather, they have been quite busy expanding their loans and securities. As shown in Chart 1, bank credit (loans and securities) has increased at a compound annual growth rate (CAGR) of 6.2% in the three months ended February 2014. Since the beginning of the current economic recovery/expansion, this is the fastest 3-month growth in bank credit since the 6.1% in the three months ended November 2011. Year-over-year, of course, growth in bank credit is considerably more subdued, but it has accelerated from 0.9% in the 12 months ended December 2013 to 1.6% in the 12 months ended February 2014 (see Chart 1).

Chart 1

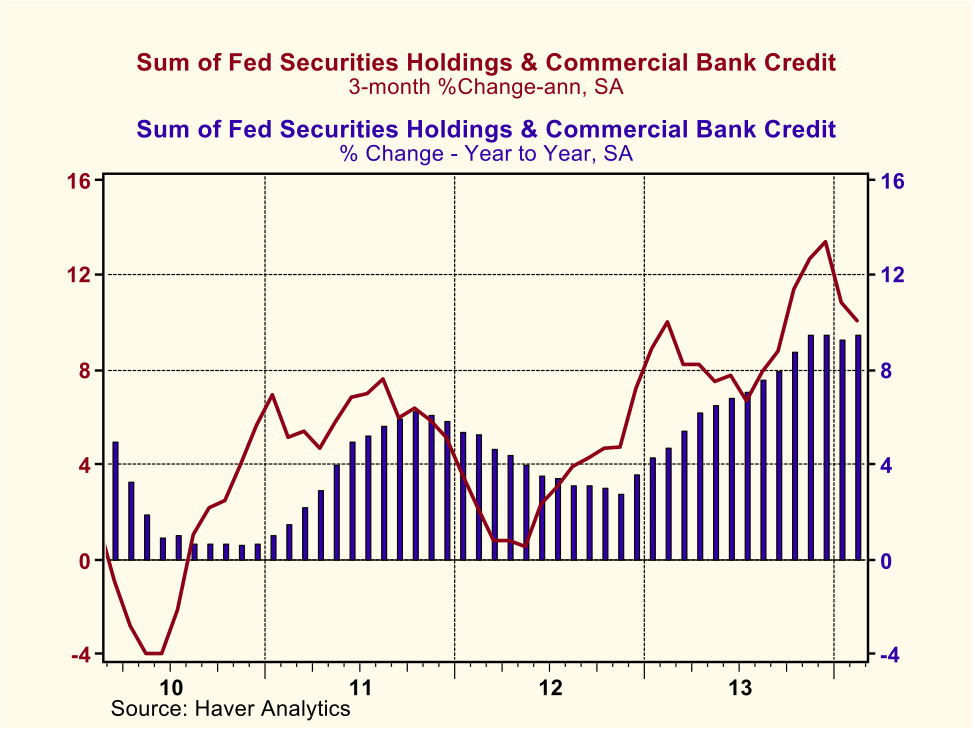

For domestic spending on goods, services and assets, real and financial, this acceleration in bank credit is coming at a good time inasmuch as Fed credit creation is slowing. As you no doubt are aware, the Fed announced at its December 2013 FOMC meeting that it would “taper” its securities-purchase program of approximately $85 billion per month to $75 billion per month starting in January 2014. Fed officials have indicated that that the Fed currently plans to continue tapering its securities-purchase program by $10 billion per FOMC meeting in 2014, depending, of course, on the Fed’s perception of the pace of economic activity. According to my reckoning, by December 2014, the Fed will have ceased outright purchases of securities if it sticks to its current tapering schedule. So, on a monthly basis, let’s see what the behavior has been of the sum of Fed credit (here defined as Fed securities holdings, outright and repurchase agreements) and commercial bank credit. Despite the acceleration in bank credit, Fed tapering has slowed the three-month growth in the sum of Fed securities holdings and bank credit. As shown in Chart 2, in the three months ended February 2014, this credit sum has increased at a CAGR of 10.1%, down from the CAGR of 13.4% in the three months ended December 2013, prior to the Fed’s commencement of tapering. But even with this deceleration in growth, an annualized growth rate of 10.1% still is quite high when compared with a long-run median annualized growth rate of about 7-1/2% for the sum of Fed securities holdings and bank credit.

Chart 2

On a year-over-year basis, Fed tapering has yet to have any deceleration effect on growth in the sum of Fed securities holdings and bank credit. Also as shown in Chart 2, February 2014 year-over-year growth in this credit sum was 9.5%, the same as that of December 2013.

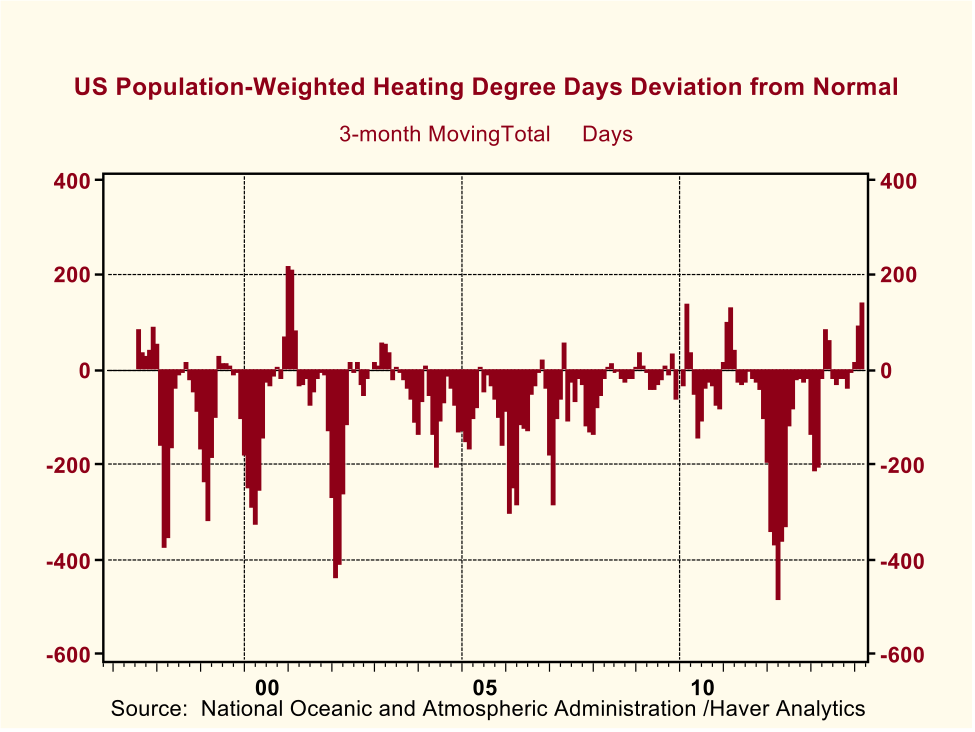

If growth in the principal component of “thin-air” credit, the sum of Fed securities holdings and commercial bank credit has been so strong of late, why have elements of domestic spending on goods and services been so weak? Perhaps the colder-than-normal winter weather? Chart 3 shows the three-month-moving-total deviation from normal heating-degree days. (A heating-degree day, HDD, is a quantitative index which reflects heating energy requirements, i.e. demand for energy to heat houses and businesses or to grow crops. It is defined as 65-MT=HDD, where 65 is the base temperature and MT is Mean Temperature (average of high and low). If MT is equal to or greater than 65 degrees, HDD=0.) In the three months ended February, the cumulative total of HDDs above normal was 146 days. Although the Februarys of 2010 and 2011 come close, this recent February has been the highest three-month ended February cumulative number of above-normal HDDs (whew!) since the 1997 inception of the (Haver Analytics) data series. The three months ended December 2000 and January 2001 had higher HDD deviations, but the three months ended February 2001 does not hold a candle to that of February 2014.

Chart 3

This extremely cold weather has kept people away from the malls, restaurants, car dealerships and model homes. And then there has been the snow, which has negatively affected these just-mentioned spending opportunities and also has disrupted the supply side of things, such as air travel. Heck, as this is being written, all non-essential federal government workers in D.C. are at home because of a snowstorm. This is the fifth snow-day this year for D.C. federal workers. Think of the loss of production there. Okay, bad example.

Of course, while some expenditures have been depressed by the nasty winter weather, others have been strengthened, such as spending on heating and snow removal. (I had to pay a grand to have the snow shoveled off my roof! And this winter may have done in my 1995 Subaru. Right now, I am awaiting a diagnosis from my mechanic to find out if it is terminal. Say a bracha for it, will you?) But all in, I believe the worse-than-normal winter weather has held back economic activity in the first quarter.

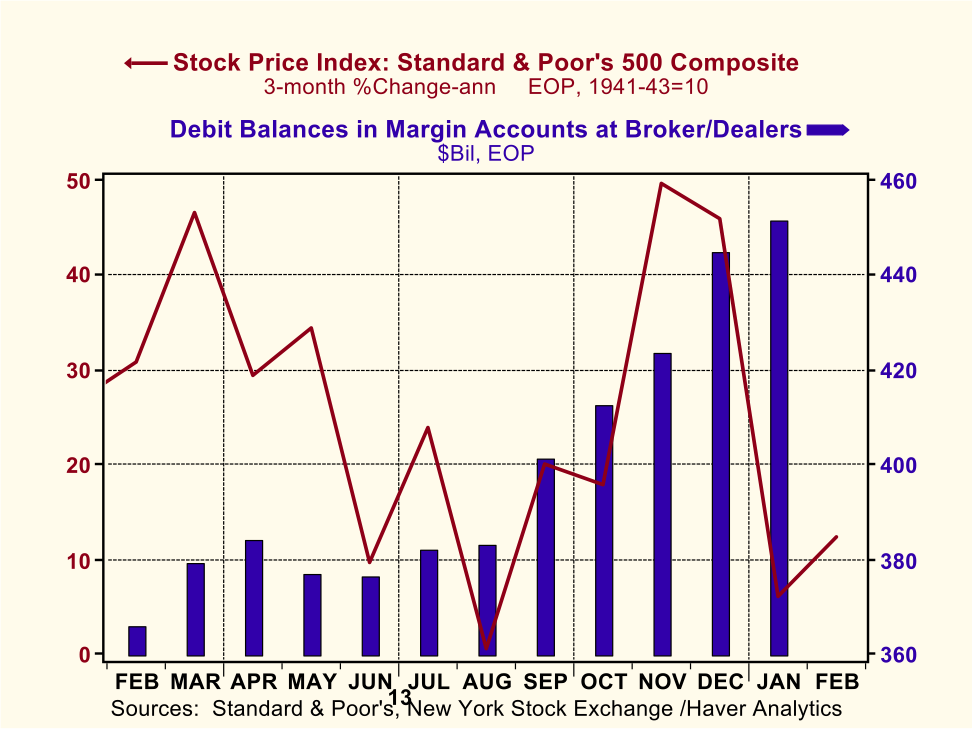

The bad weather should not have kept people from borrowing to purchase risk assets such as equities. And the rise in stock market margin debt through January 2014 indicates that some of the increased bank credit was used to purchase equities. But, as shown in Chart 4, the rate of advance in U.S. equity prices in the three months ended January and February 2014 slowed from the late fall of 2013. Blame it on China. When the second largest economy in the world shows signs of slowing, global risk investors get jittery.

Chart 4

Concerns about the Chinese economy will persist into the second and third quarters of this year, but the harsh winter weather in the northern hemisphere will be just a bad memory. So, given the strong growth in the sum of Fed securities and bank credit in recent months and the likely continued strong growth in this credit sum until the fourth quarter of this year, I expect that growth in nominal domestic spending is going to accelerate significantly in the second and third quarters of 2014. Barring safe-haven buying of Treasury securities due to geo-political events (Russia? Iran?), investment-grade bond yields will rise, with the yield on the 10-year Treasury approaching 3%. Fed hawks will start displaying their talons. Despite “forward guidance” to the contrary by Fed doves, short-term interest rates also will rise as the market expectations regarding the first Fed rate hike will be brought forward. The higher interest rate structure will offer resistance to the equity markets. But I believe equity prices can still move higher, albeit at a subdued pace, with the help of continued strong growth in thin-air credit and strengthening domestic demand for goods and services.

Things get dicier, however, toward the end of 2014 and into 2015 as the full effects of Fed tapering come into play. Plotted in Chart 5 are the year-over-year percent changes of monthly observations of the sum of Fed securities holdings (outright and repurchase agreements) and commercial bank credit. Actual historical data are plotted through February 2014, projections thereafter. There are two scenarios in the projection plots. Scenario I assumes that bank credit continues to grow at its current three-month CAGR of 6.2% and the Fed tapers its securities purchases such that net purchases are zero in December 2014 and remain so through 2015. Scenario II is the same as Scenario I except that starting in January 2015, the Fed increases its securities holdings every month at a CAGR of 7.0% — the median Q4/Q4 percent change in Fed securities holdings (outright and repurchase agreements) from 1954 through 2006. So, the two scenarios are identical until January 2015.

Chart 5

In February 2014, the year-over-year growth in this credit sum was 9.5%. Starting in March 2014 through September 2014, the year-over-year growth in this credit sum stays in a range of 9.2% to 9.5% under my scenarios. But year-over-year growth in this credit sum begins slowing in the fourth quarter of 2014, and by December 2014, year-over-year growth is 7.7%. Now, 7.7% annual growth in the sum of Fed securities holdings and bank credit is not weak in absolute terms. After all, the long-run median annual growth rate of this credit sum is around 7-1/2%. But a deceleration in growth from 9.5% to 7.7%, almost 200 basis points, is not insignificant. Given about a one-quarter lag between year-over-year changes in thin-air credit and year-over-year changes in nominal domestic spending on goods and services, the effect on nominal demand growth might be only marginal in the fourth quarter of 2014.

Under Scenario I, the Fed securities holdings remain constant throughout 2015, with bank credit increasing monthly at a CAGR of 6.2%. Under this scenario, by June 2015, the year-over-year percent change in the sum of Fed securities holdings and bank credit has slowed to 5.1%. By December 2015, it has slowed to 4.4%. Scenario I would represent a significant tightening in monetary policy, which would be bearish for equities. As I expect yields on investment grade bonds to be rising in 2014, I would think that, at worst, bond yields would stabilize at their higher end-of-2014 levels. At best, bond yields would decline some in 2015. Under normal circumstances, which I think these would be, the Fed can control either the quantity of bank reserves (related closely to the quantity of securities held by the Fed) or the price of reserves, the fed funds rate – but not both simultaneously. So, I believe that Scenario I would imply a rise in the fed funds rate above its current target range of zero-to-1/4%.

As I just said, the Fed can control either the quantity of reserves or the fed funds rate. In the post-WWII era, with some minor exceptions, the Fed has chosen to control the fed funds rate, adjusting the quantity of bank reserves (and its holdings of securities) to whatever level necessary to hit its fed funds target. This has worked out to a median year-over-year percent change in Fed securities holdings (including securities held via repurchase agreements) of 7.0%. So, for Scenario II, which I believe is more likely than Scenario I, I have assumed that the Fed will go back to “normal” with regard to the growth in its securities holdings. (As an aside, Fed securities holdings increased 40.7% December 31, 2013 vs. December 31, 2012.) With Fed securities holdings (including repurchase agreements) increasing monthly at a CAGR of 7.0% and bank credit increasing at a CAGR of 6.2%, by June 2015, the year-over-year growth in this credit sum would be 6.2%. By December 2015, under Scenario II the year-over-year growth in this credit sum would be 6.5%. Scenario II, then, also would represent a tightening in monetary policy, but not as severe a tightening as Scenario I. Similarly, the fed funds rate would likely move higher in 2015 under Scenario II, but not as much as under Scenario I. Under Scenario II, both equities and investment grade bonds would experience a lot of volatility with little trend.

One last point. Sustained annualized growth in the sum of Fed securities holdings and bank credit at 9-1/2% is bubblicious. This is what brought us the NASDAQ bubble of the late 1990s and the housing bubble of mid 2000s, also what I call “Greenspan’s legacy”. In order to avoid yet another bubble (yes, I know, the nattering nabobs of negativism who are disappointed we did not relive the Great Depression think we already are in a new bubble economy), it is entirely proper that growth in thin-air credit slow in 2014. If growth in bank credit is accelerating, then growth in Fed credit needs to decelerate in order to bring down the growth in the sum of Fed and bank credit to a less bubblicious rate. If only the Fed would take Milton Friedman’s advice to abandon its obsession with targeting the price of thin-air credit and adopt a policy of targeting/controlling the quantity of thin-air credit, then we could avoid asset-price bubbles and bouts of consumer inflation or deflation.

Paul L. Kasriel

Econtrarian, LLC

Senior Economic and Investment Advisor

Legacy Private Trust Co., Neenah, WI

econtrarian@gmail.com

1-920-818-0236

What's been said:

Discussions found on the web: