Is the Bull Dead?

Is the bull market, which started after the lows of early 2009, coming to an end? Let’s have a look at some data, as well as the...

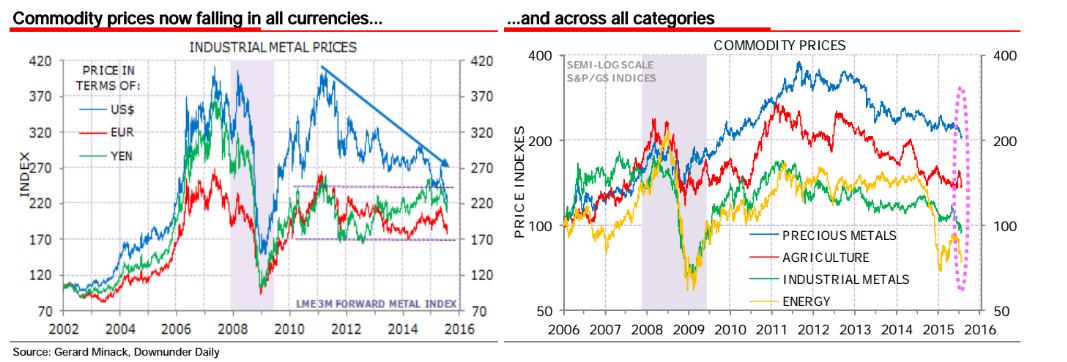

…and across all categories Source: Gerard Minack, Downunder Daily

…and across all categories Source: Gerard Minack, Downunder Daily

Nice chart from WSJ about the stockpiles of foodstuffs around the world: Source: WSJ

Nice chart from WSJ about the stockpiles of foodstuffs around the world: Source: WSJ

Back in March, I posted some info on Crude passing $105 and hitting $107 for the first time: Crude Oil = $107. Its a round trip: We...

Back in March, I posted some info on Crude passing $105 and hitting $107 for the first time: Crude Oil = $107. Its a round trip: We...

GDP Deflator versus CPI click for larger chart chart courtesy of Eric Jantzen > In our exploration of how laughable the 3.3% GDP was...

GDP Deflator versus CPI click for larger chart chart courtesy of Eric Jantzen > In our exploration of how laughable the 3.3% GDP was...

Back in July, I noted that we had exited many energy positions, and would like to see Oil pull back to $105-110 to re-enter them. This...

Back in July, I noted that we had exited many energy positions, and would like to see Oil pull back to $105-110 to re-enter them. This...

Get subscriber-only insights and news delivered by Barry every two weeks.