Next week I walk into the lion’s den to explain to crypto true believers why they need to bring the same level of...

Next week I walk into the lion’s den to explain to crypto true believers why they need to bring the same level of...

Read More

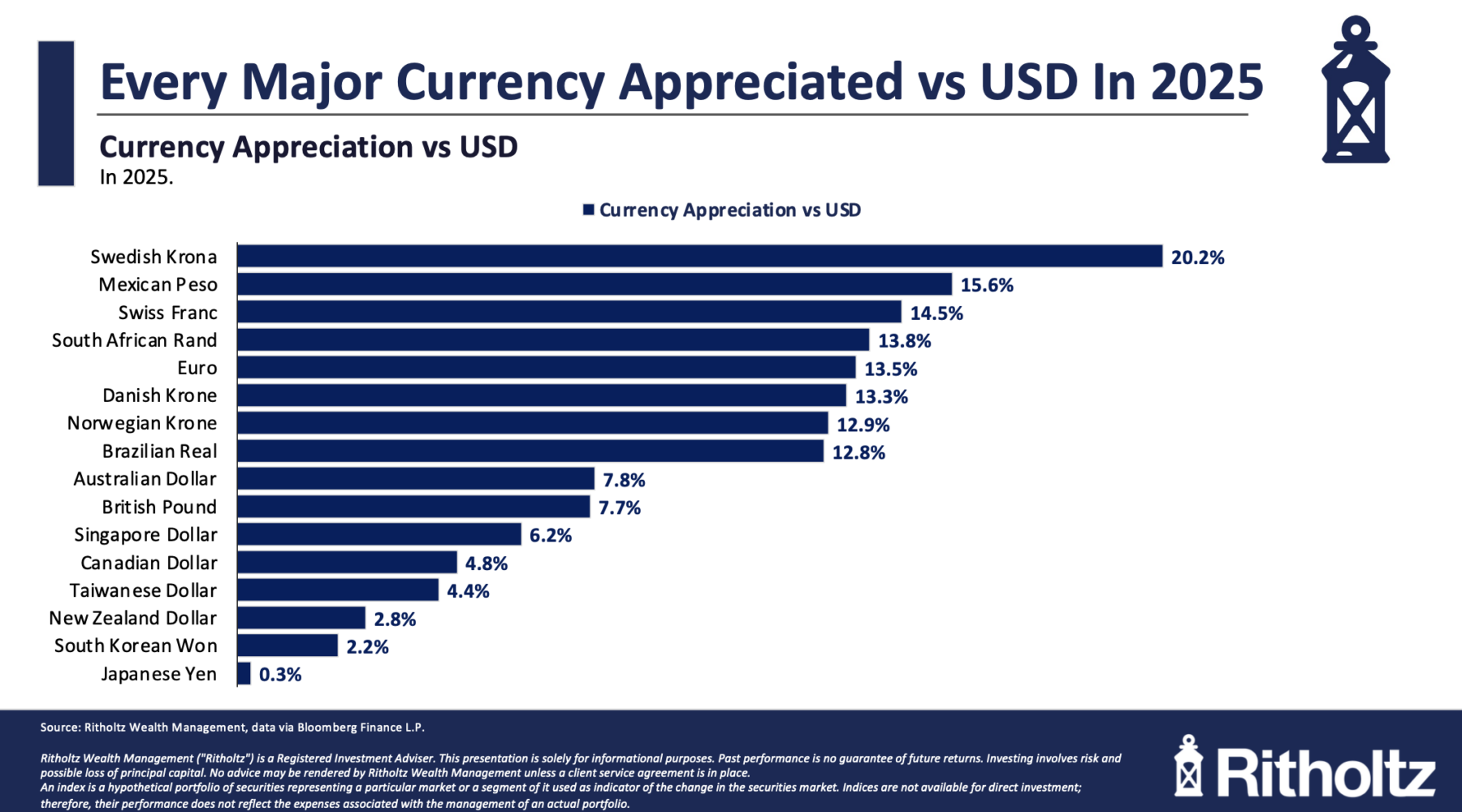

I am always searching for interesting and informative charts, especially ones I can include in my quarterly call, that...

I am always searching for interesting and informative charts, especially ones I can include in my quarterly call, that...

Read More

At The Money: How Greed Became a Virtue. (September 24, 2025) It’s a driving factor in our lives. But how often have you...

Read More

At The Money: Paul Vigna explains “What is Money?” (August 6, 2025) It’s a driving factor in our lives....

Read More

At the Money: Crypto Curious. November 26, 2024 Are you crypto-curious? Are you interested in owning some bitcoin,...

Read More

“I need the US Dollar to be a store of value between the time I make it until I spend it, invest it, pay my...

“I need the US Dollar to be a store of value between the time I make it until I spend it, invest it, pay my...

Read More

Barry Ritholtz, a Bloomberg Opinion columnist, talks Bitcoin and Banks with Bloomberg’s Tom Keene and Lisa Abramowicz on...

Read More

This week, we speak with Duke University finance professor Campbell Harvey. Since 2014, his Fuqua School of Business...

Read More

A friend accidentally sent me an invite to a metals and mining conference. She knows I was bullish on Gold in the mid-2000s...

A friend accidentally sent me an invite to a metals and mining conference. She knows I was bullish on Gold in the mid-2000s...

Read More

I weigh in on the cryptocurrency debate with Tom Keene and Lisa Abramowicz Bitcoin ‘Lacks Teeth’ of Traditional...

Read More