The Libertarian Ideas That Wrecked the Fed Milton Friedman’s influence on America’s monetary policy blew up the past and mortgaged...

The Libertarian Ideas That Wrecked the Fed Milton Friedman’s influence on America’s monetary policy blew up the past and mortgaged...

Read More

This week, we speak with Claudia Sahm, former Section Chief at the Board of Governors of the Federal Reserve System, and Senior Economist...

Read More

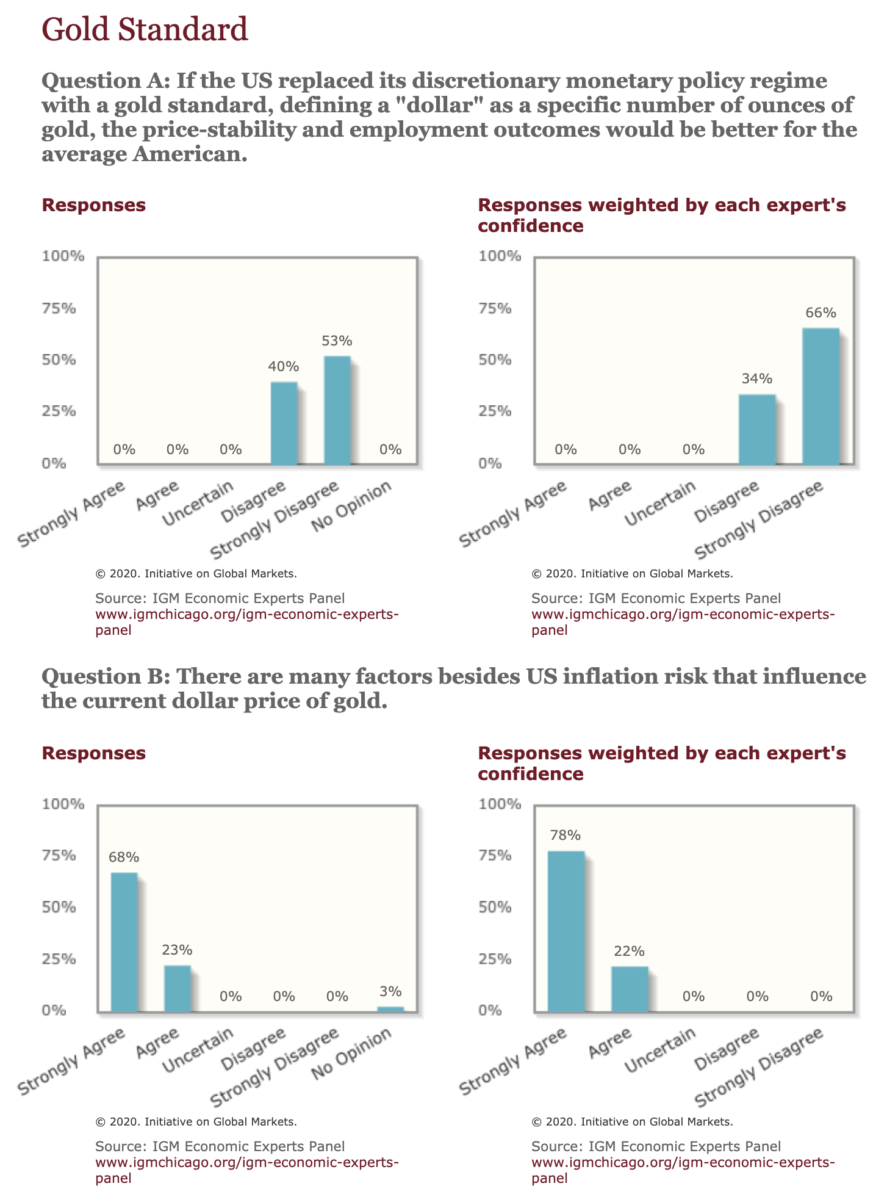

If the president gets his way, Judy Shelton will bring crackpot goldbuggery back to the central bank. This week, the Senate...

If the president gets his way, Judy Shelton will bring crackpot goldbuggery back to the central bank. This week, the Senate...

Read More

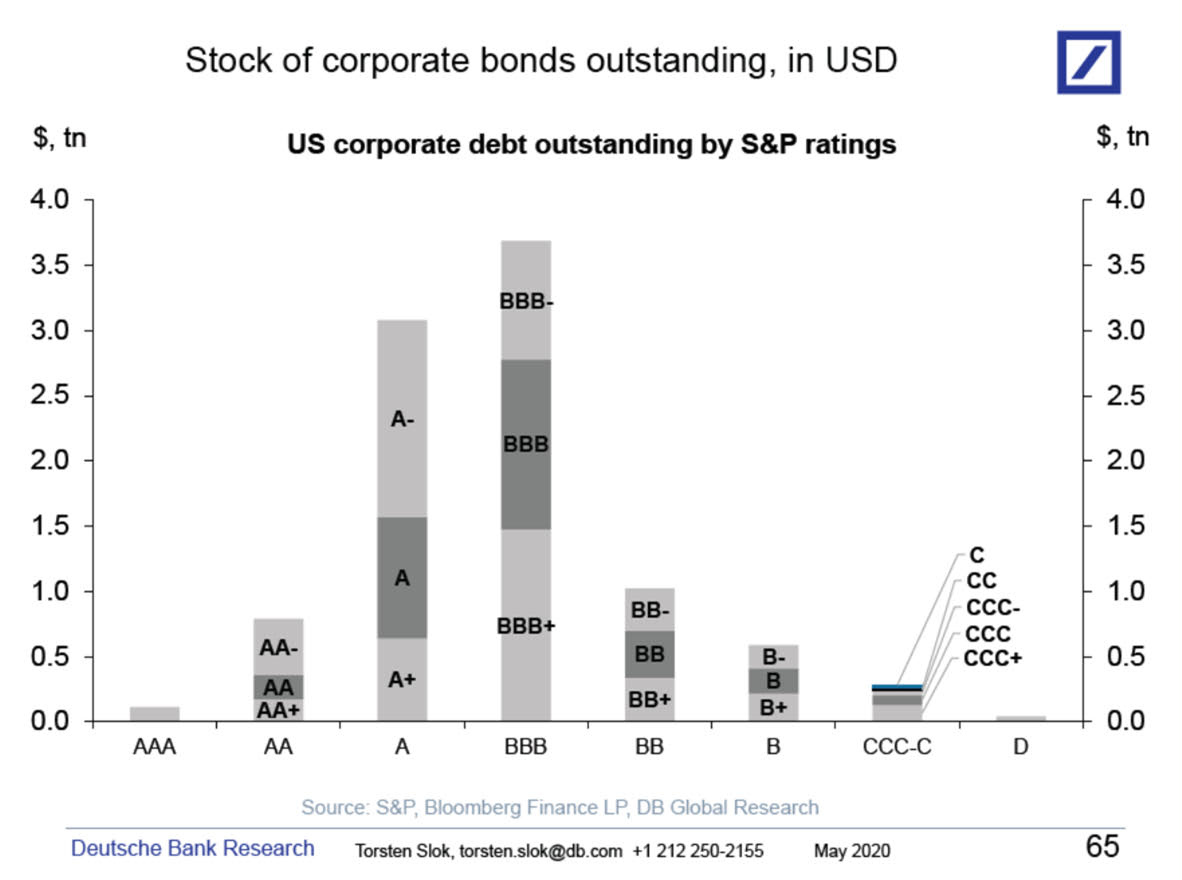

Negative interest rates not the right tool for this shock Source: Torsten Sløk, Deutsche Bank Research Torsten Sløk, chief...

Negative interest rates not the right tool for this shock Source: Torsten Sløk, Deutsche Bank Research Torsten Sløk, chief...

Read More

The head of the U.S. central banking system tells Scott Pelley how high he thinks unemployment will go, what tools the Fed still has to...

Read More

The Coronavirus pandemic has led to an unprecedented economic collapse, both here and around the globe. The Federal Reserve responded by...

Read More

This week, we speak with Christopher Whalen, an investment banker and former Federal Reserve researcher. He is the founder of Whalen...

Read More

In an extraordinary attempt to help the economy in the midst of a pandemic-driven economic downturn, the Federal Reserve’s balance...

Read More

The former Treasury official who was in charge of the $700 billion government response to the 2008 financial crisis tells 60 Minutes what...

The former Treasury official who was in charge of the $700 billion government response to the 2008 financial crisis tells 60 Minutes what...

Read More

What should you do about an interventionist central bank that pretends to be a laisse faire regulator? That was the main topic in our...

Read More