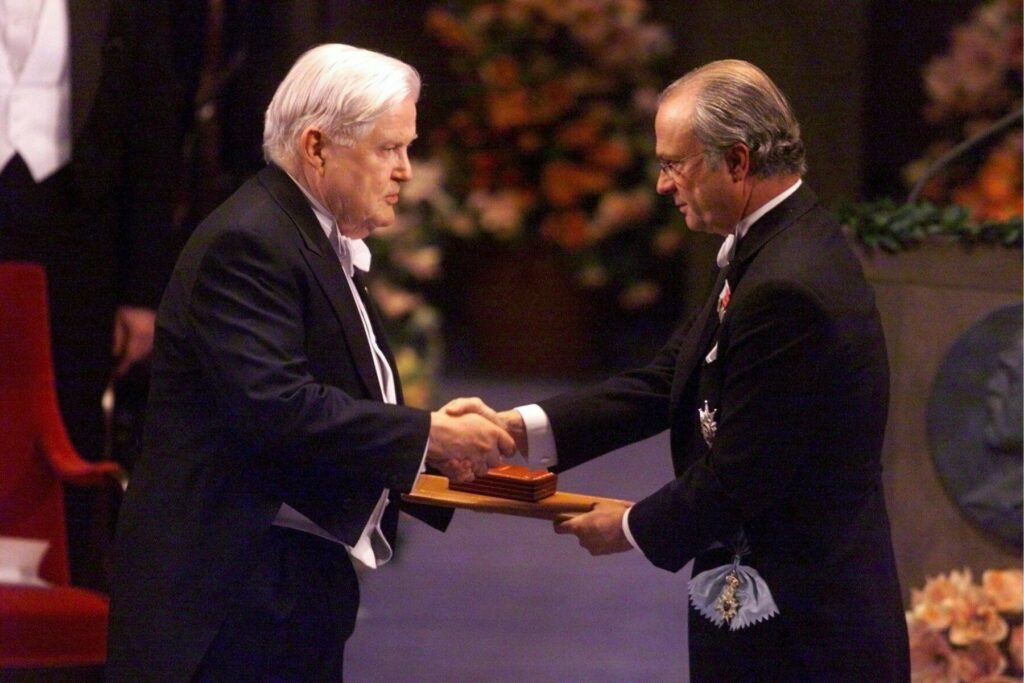

Remembering the Father of Supply-Side Economics Robert Mundell’s theories spawned decades of economic debate and still...

Remembering the Father of Supply-Side Economics Robert Mundell’s theories spawned decades of economic debate and still...

Read More

Socialism Is as American as Apple Pie The ideology that Republicans love to hate is woven through the fabric of the...

Socialism Is as American as Apple Pie The ideology that Republicans love to hate is woven through the fabric of the...

Read More

40 years ago, Isaac Asimov, one of America’s best known writers, explained the issue with both-sides-ism. “It’s hard to...

Read More

Here is a shocking observation: The pandemic lockdown began in March of 2020. As of today, the two leading vaccine candidates from...

Here is a shocking observation: The pandemic lockdown began in March of 2020. As of today, the two leading vaccine candidates from...

Read More

Election day is finally here. Last month, I shared some random facts related to markets and the election. Here are some more small items...

Election day is finally here. Last month, I shared some random facts related to markets and the election. Here are some more small items...

Read More

Yesterday’s column, Mediocre SPAC Returns Shouldn’t Be a Surprise, was ostensibly about special-purpose acquisition...

Yesterday’s column, Mediocre SPAC Returns Shouldn’t Be a Surprise, was ostensibly about special-purpose acquisition...

Read More

How Corporations Pillaged the Free Market Milton Friedman’s siren song of profit convinced lawmakers to stop worrying about people and...

How Corporations Pillaged the Free Market Milton Friedman’s siren song of profit convinced lawmakers to stop worrying about people and...

Read More

The 10 Most Useless Phrases in Financial Markets Catchy slogans are not only no substitute for critical analysis, they are often wrong....

The 10 Most Useless Phrases in Financial Markets Catchy slogans are not only no substitute for critical analysis, they are often wrong....

Read More

Never shared this story about Bill Meehan before but today is a day to remember. #RIP @billmeehan @jimcramer...

Never shared this story about Bill Meehan before but today is a day to remember. #RIP @billmeehan @jimcramer...

Read More

Brexit, Facebook, Endowments and Other Errors Acknowledging mistakes increases the odds of avoiding them in the future. Bloomberg,...

Read More