click for ginormous chart While I am wrapped up working on a few projects today, I wanted to share this map/chart/table showing US...

click for ginormous chart While I am wrapped up working on a few projects today, I wanted to share this map/chart/table showing US...

Read More

My buddy Jonathan Miller does not hesitate to call out the weasels who represent those who work in his industry: NAR Proves...

My buddy Jonathan Miller does not hesitate to call out the weasels who represent those who work in his industry: NAR Proves...

Read More

The transcript from this week’s, MiB: Jonathan Miller on Post-Pandemic Residential Real Estate, is below. You can stream...

Read More

This week, we speak with Jonathan Miller, founder and CEO of Miller Samuel, a real estate...

Read More

Source: Reventure Let’s get to the caveats up front: Re:Ventures has been pretty bearish on housing the past few years, even...

Source: Reventure Let’s get to the caveats up front: Re:Ventures has been pretty bearish on housing the past few years, even...

Read More

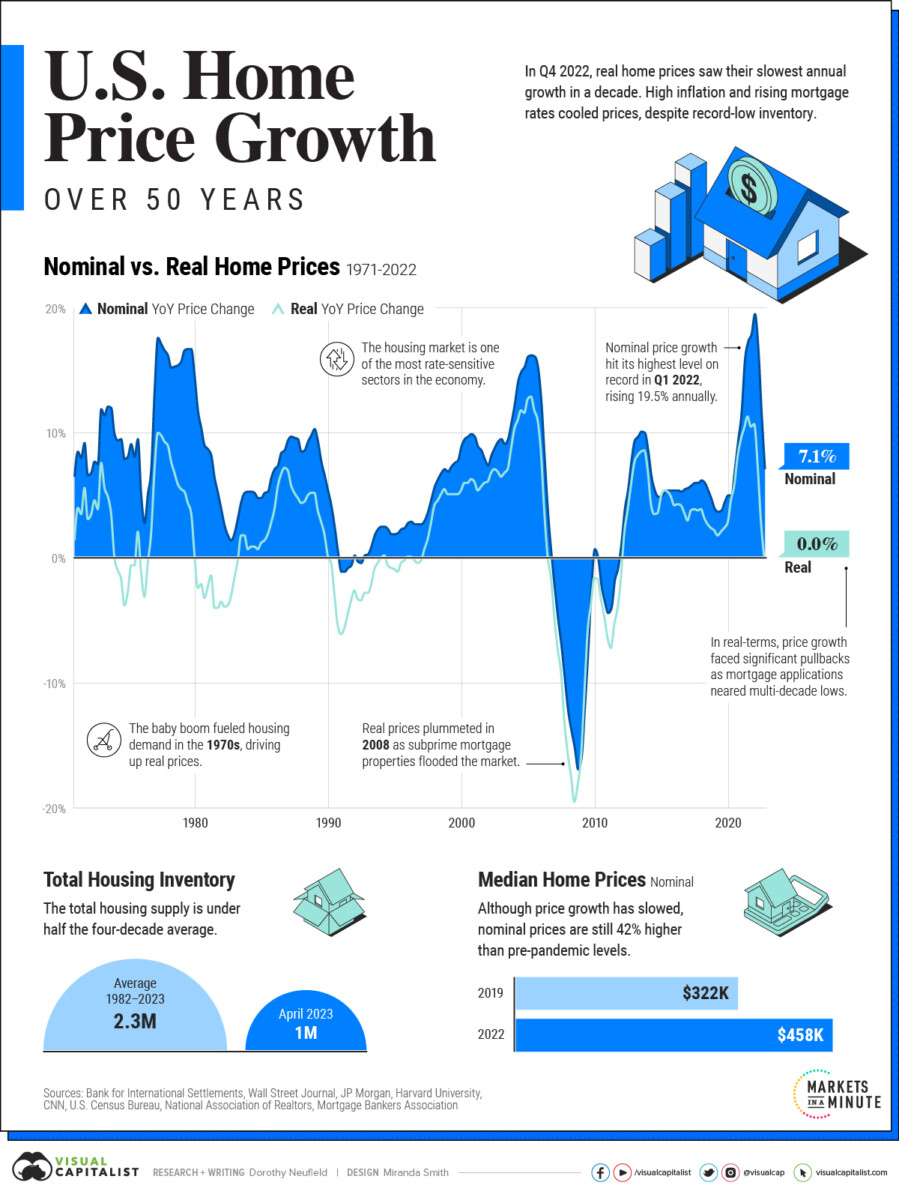

Fascinating chart from Visual Capitalist showing the history of housing prices in the United States. I recall the 1990 Home Price...

Fascinating chart from Visual Capitalist showing the history of housing prices in the United States. I recall the 1990 Home Price...

Read More

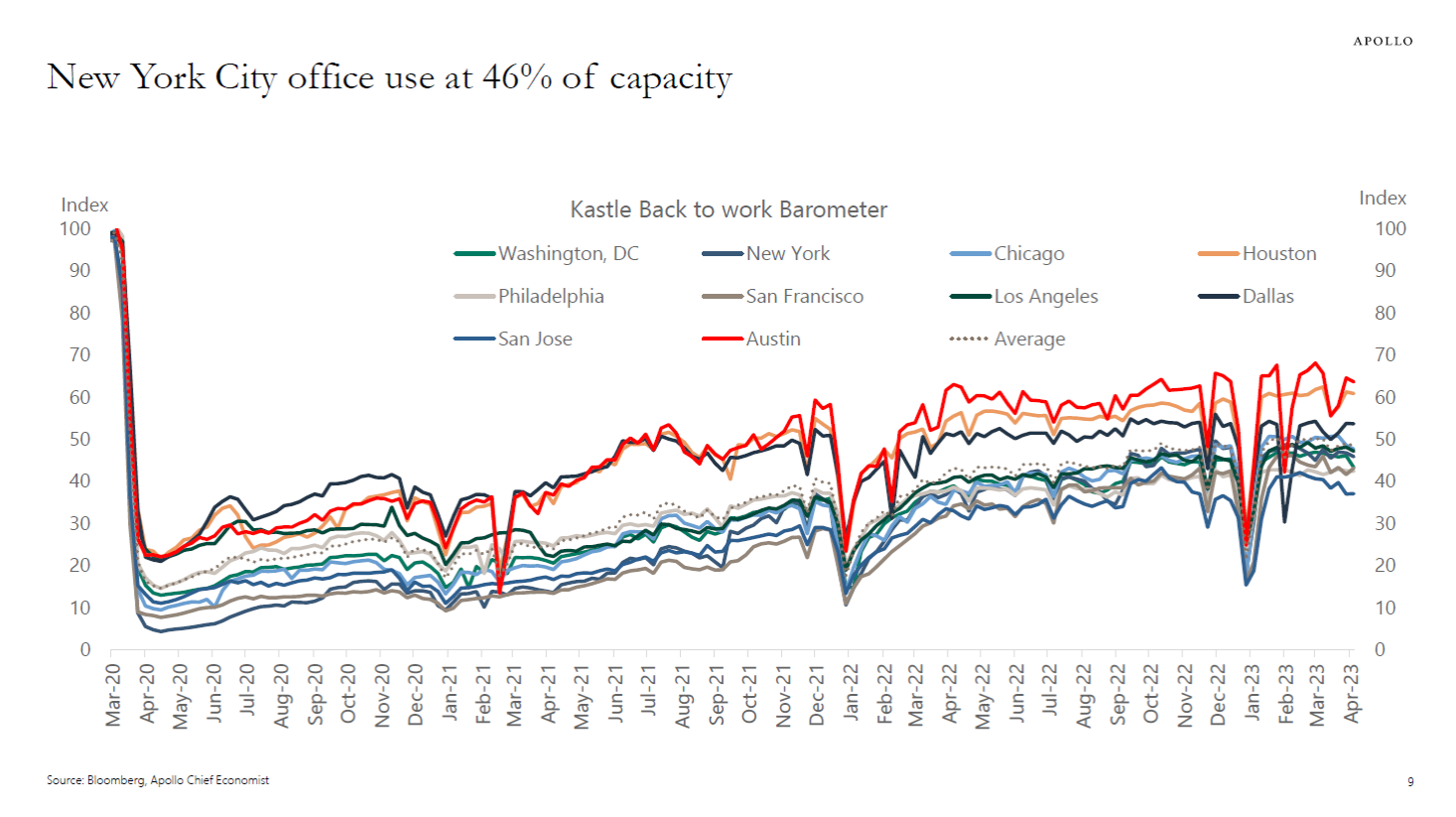

I mentioned a few weeks ago how much better Europe‘s return to office rate was doing versus ours: 90+% RTO, while the USA is...

I mentioned a few weeks ago how much better Europe‘s return to office rate was doing versus ours: 90+% RTO, while the USA is...

Read More

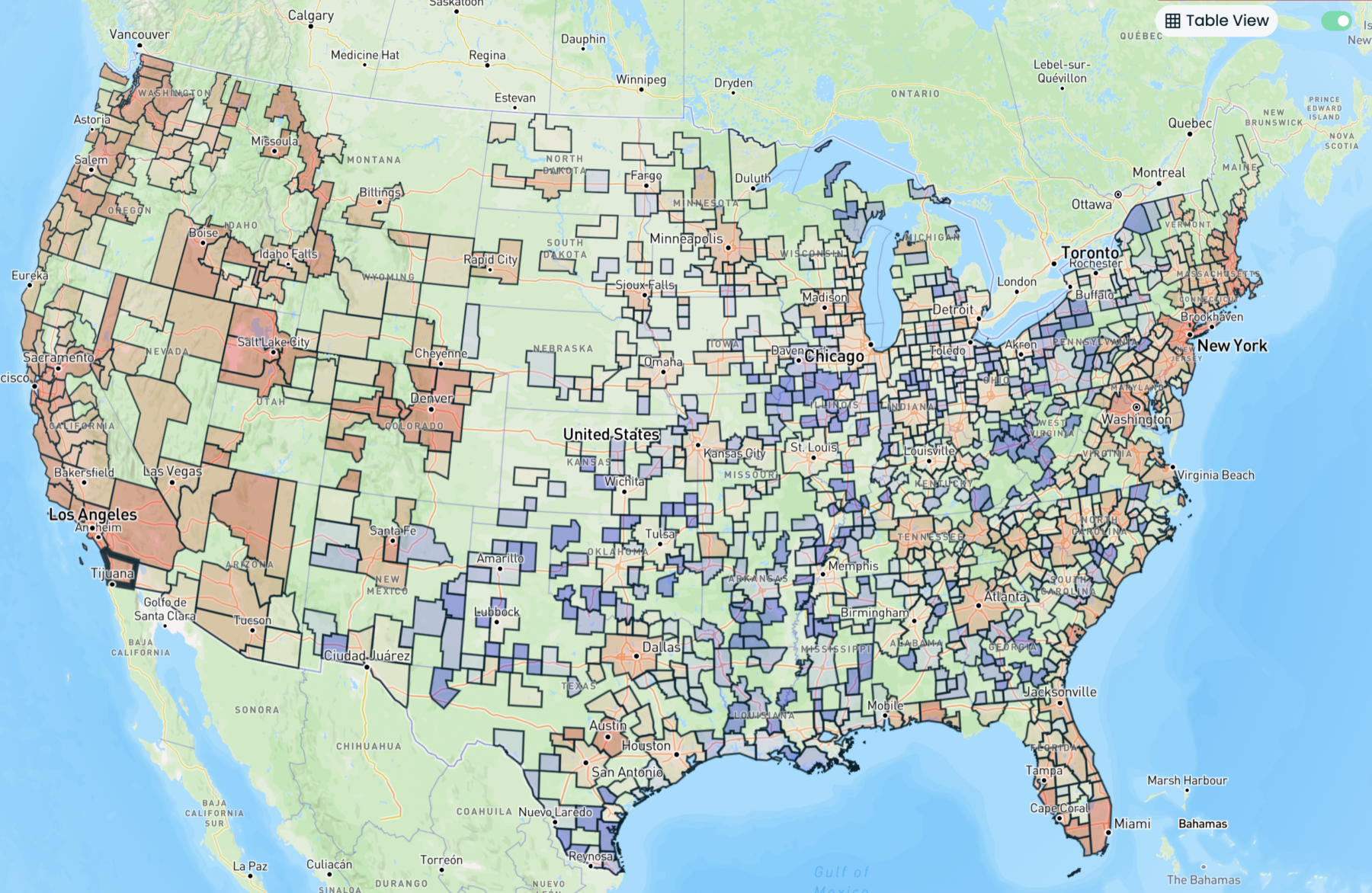

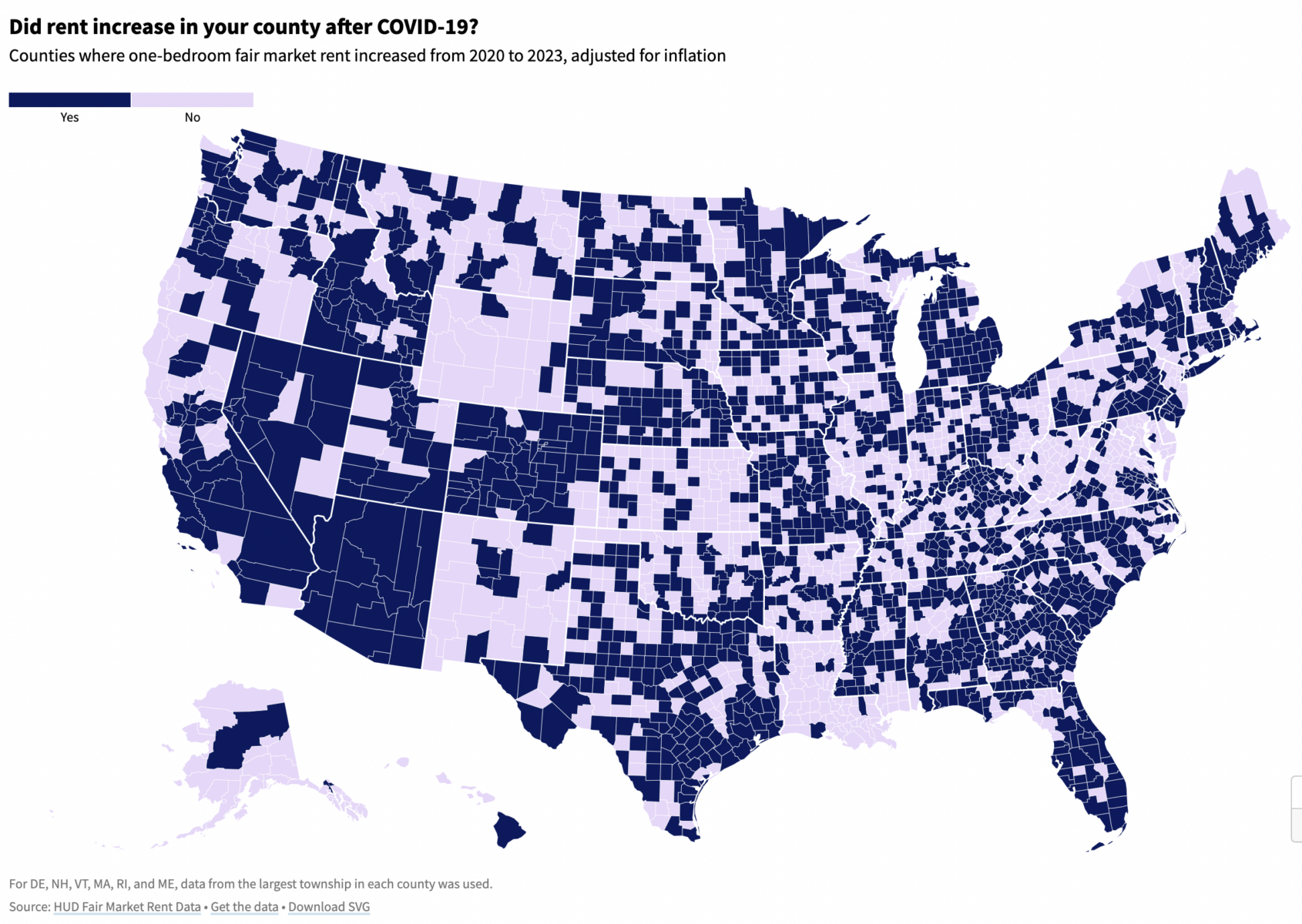

Fascinating dive into rent increases on a county by county basis via USAFacts: Rents rose in 58% of all counties nationwide...

Fascinating dive into rent increases on a county by county basis via USAFacts: Rents rose in 58% of all counties nationwide...

Read More

Today I had some fun recording portfolio rescue with Ben and Duncan. They always do a great job (I pop in around the 17-minute mark). We...

Read More