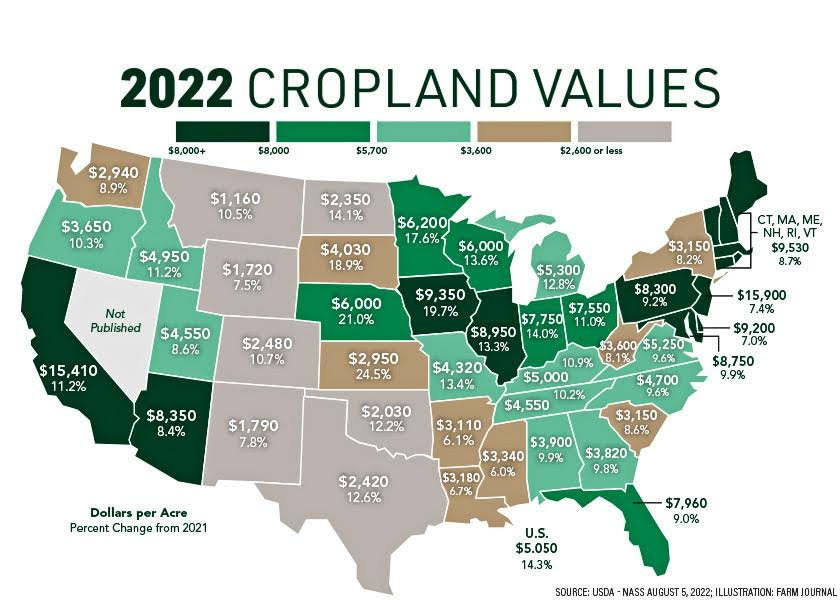

Source: AgWeb If you are interested (as I am) in Real Estate, then allow me to suggest you consider exploring the world of...

Source: AgWeb If you are interested (as I am) in Real Estate, then allow me to suggest you consider exploring the world of...

Read More

This week, we speak with Jonathan Miller, who is CEO and co-founder of the real estate appraisal and consulting firm Miller...

Read More

This one’s listed for $95m You might imagine that compromises in life ends once you accumulate a sufficient pile of...

This one’s listed for $95m You might imagine that compromises in life ends once you accumulate a sufficient pile of...

Read More

In the early days of the pandemic, lots of people (myself included) underestimated both how long Covid-19 would...

In the early days of the pandemic, lots of people (myself included) underestimated both how long Covid-19 would...

Read More

From real estate to space, Seattle’s technology scene is awash in artificial intelligence. Ashlee Vance meets Redfin Chief Executive...

Read More

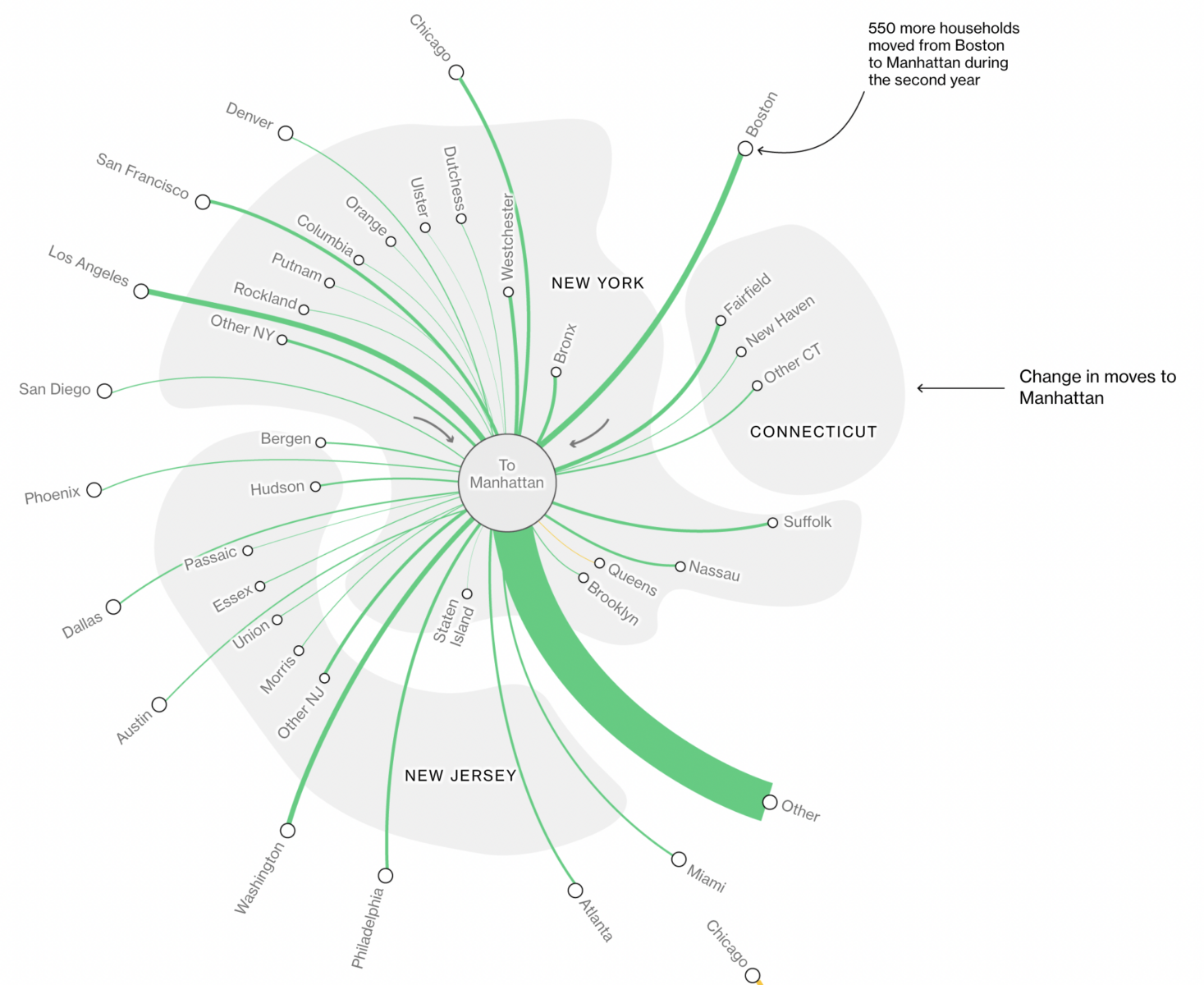

Let’s talk real estate. I am a magnet for residential real estate questions. Having more or less gotten the 2000s RRE...

Let’s talk real estate. I am a magnet for residential real estate questions. Having more or less gotten the 2000s RRE...

Read More

Luxury RE Alliance I am in Aspen Colorado presenting to a group of top-performing real estate agents. (70 agents here moved...

Luxury RE Alliance I am in Aspen Colorado presenting to a group of top-performing real estate agents. (70 agents here moved...

Read More

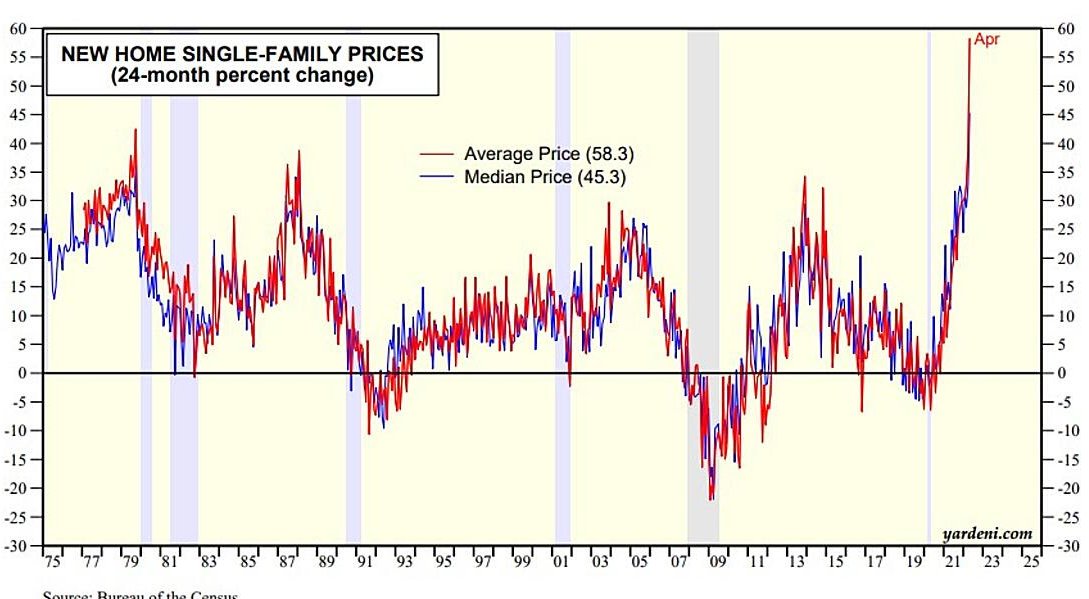

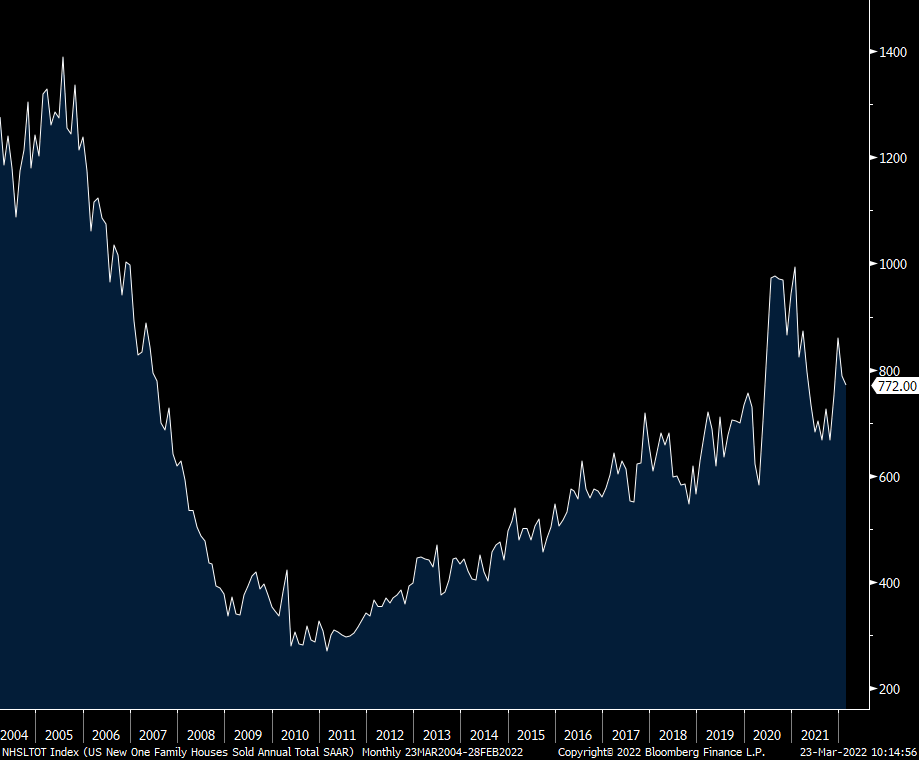

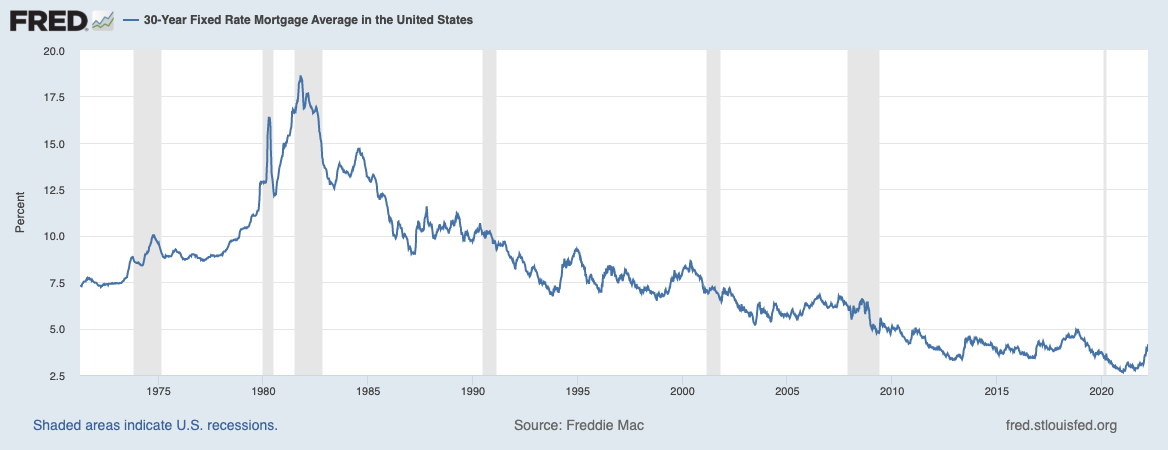

New home sales in February totaled 772k, 38k less than expected and January was revised down by 13k to 788k. Keep in mind that the...

New home sales in February totaled 772k, 38k less than expected and January was revised down by 13k to 788k. Keep in mind that the...

Read More

Would-be home buyers may be forced to rent the American dream (rather than buy it) Source: 60 Minutes Here is the key aspect of...

Read More

I have been wondering lately what the ramifications of the past two years will be. I enjoy thinking about things like this;...

I have been wondering lately what the ramifications of the past two years will be. I enjoy thinking about things like this;...

Read More