Source: WSJ

Source: WSJ

As Goes Apple, So Goes the Market?

With the stock markets down almost (OMG!) 5 percent from their all-time highs, lots of folks are looking for signs that the bull is...

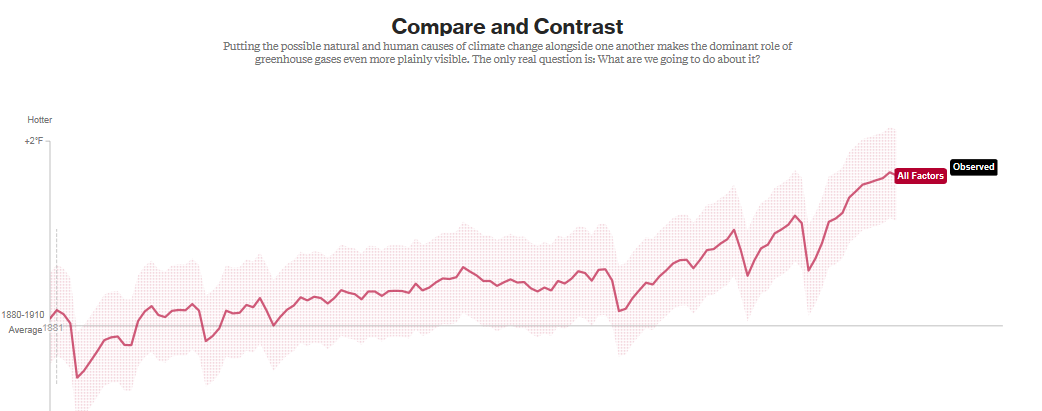

Farm-to-Table for Bad Information

@TBPInvictus I am reminded of the above law each and every day. And a law it is. Inviolable. No sooner had I posted the other day...

@TBPInvictus I am reminded of the above law each and every day. And a law it is. Inviolable. No sooner had I posted the other day...

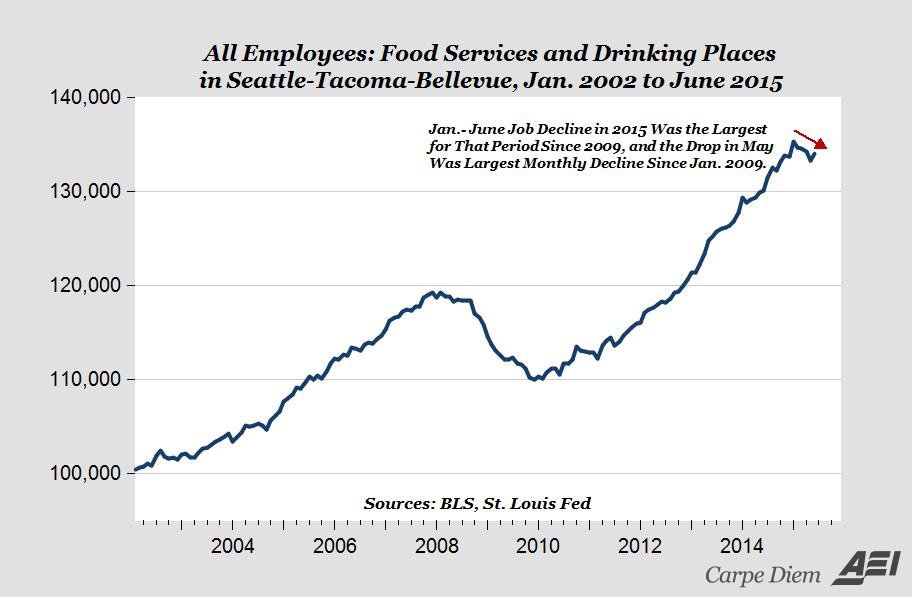

Fact Versus Fiction on Seattle Minimum Wage

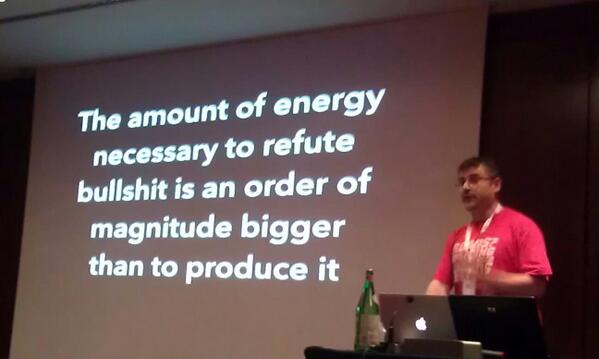

@TBPInvictus “He who knows nothing is closer to the truth than he whose mind is full of falsehoods and errors.” –...

@TBPInvictus “He who knows nothing is closer to the truth than he whose mind is full of falsehoods and errors.” –...

Sorting Through Online Investment Noise

Hey, investment cranks: The Internet never forgets By Barry Ritholtz Washington Post, August 1, 2015 As Theodore Sturgeon...

How to sort through garbage online investment advice

Who Benefits from Bailouts?

I always find it amusing whenever someone expresses surprise that the financial bailouts for Greece haven’t benefitted Greek...