Click to check out other cities. Source: Climate Central

Click to check out other cities. Source: Climate Central

Surging Seas: 2°C Warming and Sea Level Rise

Click to check out other cities. Source: Climate Central

Click to check out other cities. Source: Climate Central

Click to check out other cities. Source: Climate Central

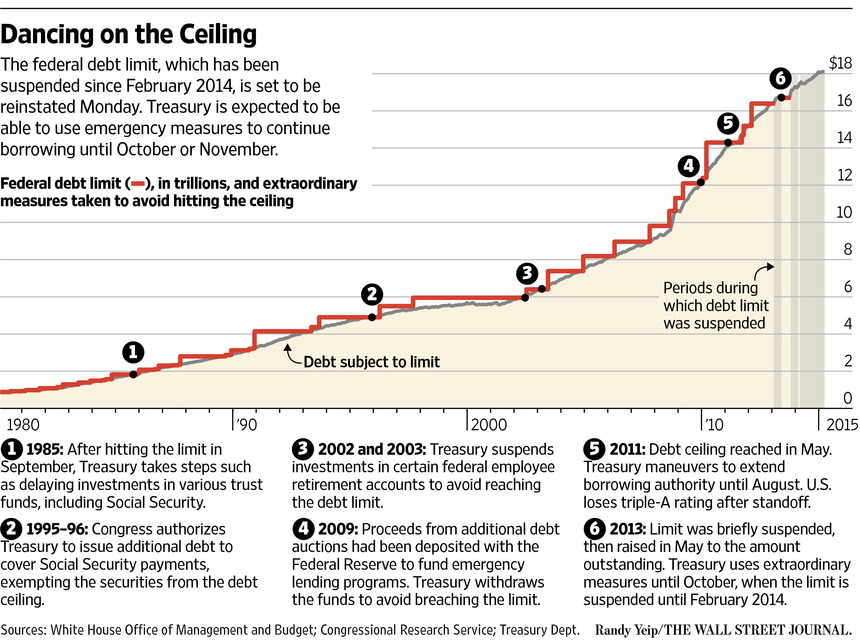

Fascinating discussion via Real Time Economics: click for ginormous graphic Source: WSJ

Fascinating discussion via Real Time Economics: click for ginormous graphic Source: WSJ

Fantastic cover from this week’s Economist; I think we have different definitions of “embrace” . . . ...

Fantastic cover from this week’s Economist; I think we have different definitions of “embrace” . . . ...

Get subscriber-only insights and news delivered by Barry every two weeks.