Playing Scrooge in “The Best Economy Ever”

@TBPInvictus here: On Presidents Day, it is noteworthy that the current President feels compelled to cap the salaries of those employees...

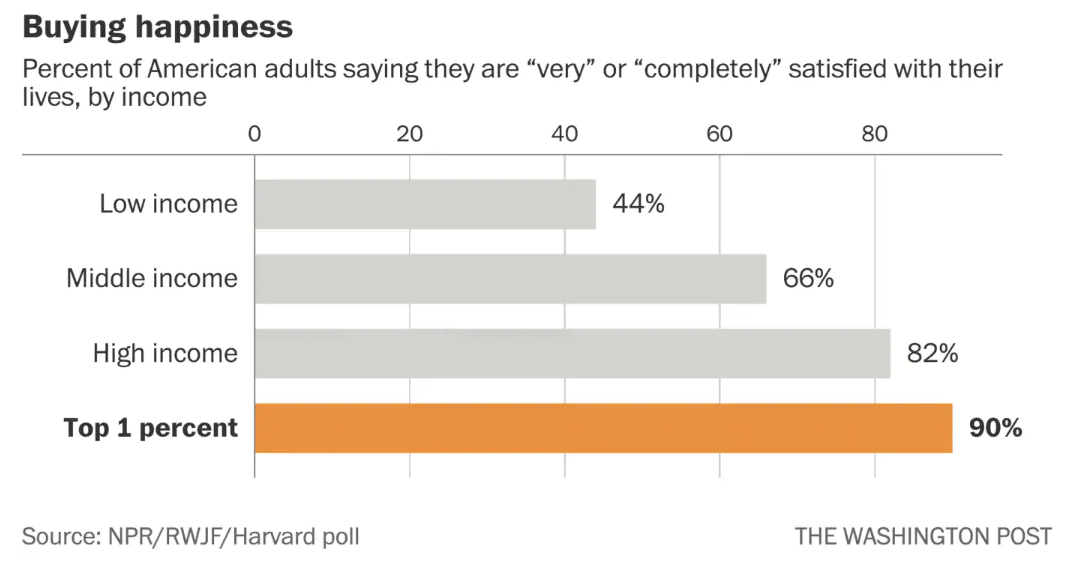

Source: Robert Wood Johnson Foundation via WaPo The past week, I have been writing about making smarter spending decisions,...

Source: Robert Wood Johnson Foundation via WaPo The past week, I have been writing about making smarter spending decisions,...

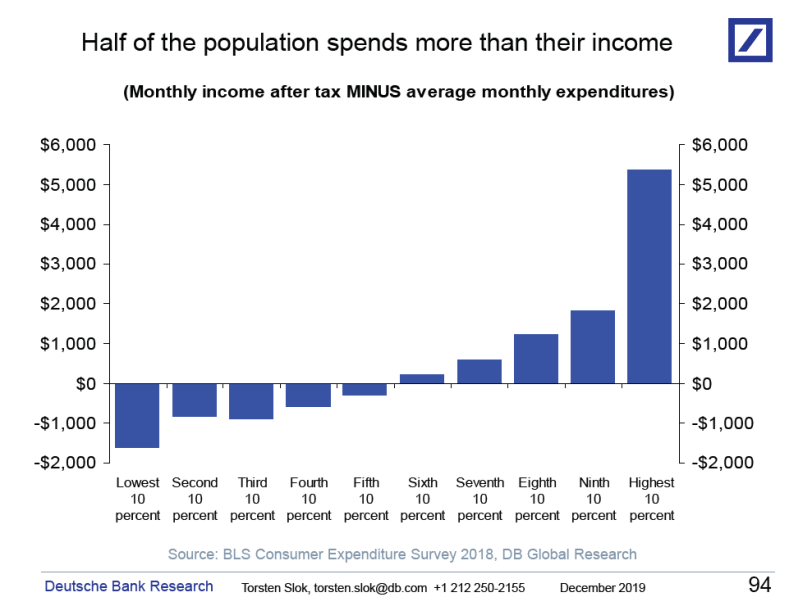

Source: Torsten Sløk, Deutsche Bank Securities Today’s Employment Situation report — up 145k jobs (mostly...

Source: Torsten Sløk, Deutsche Bank Securities Today’s Employment Situation report — up 145k jobs (mostly...

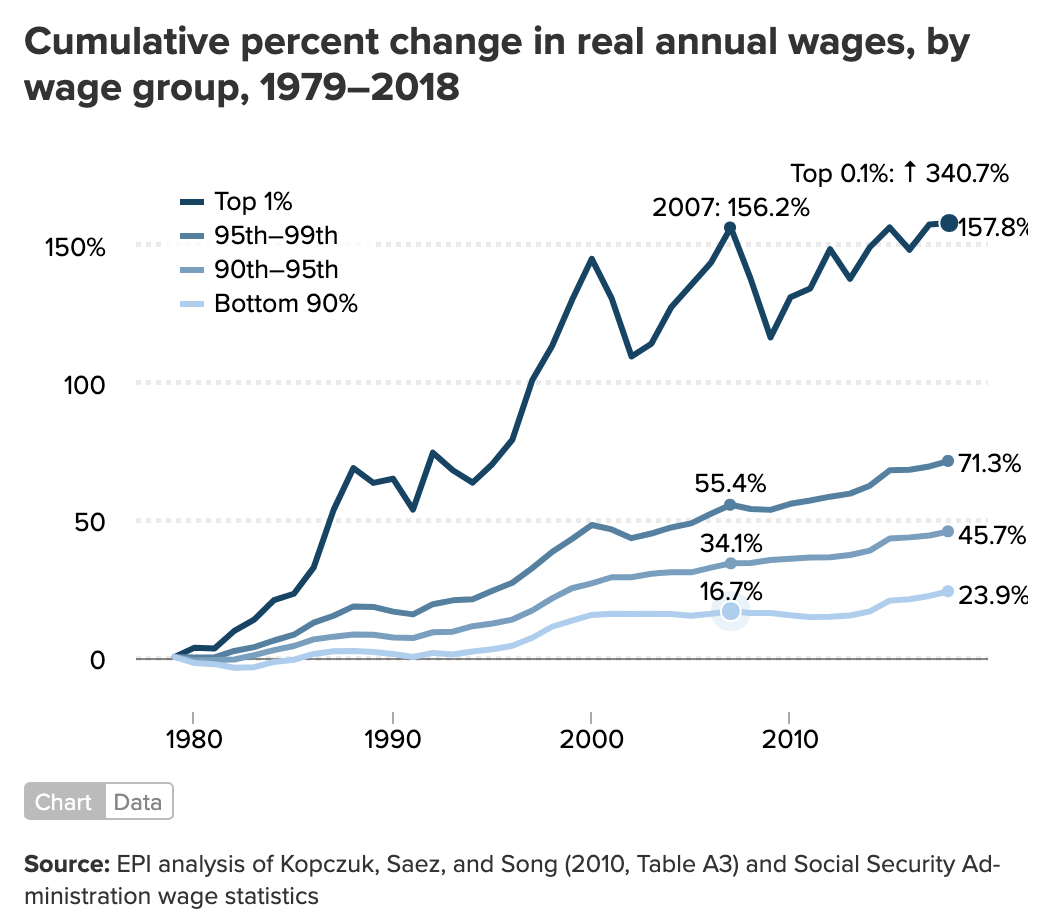

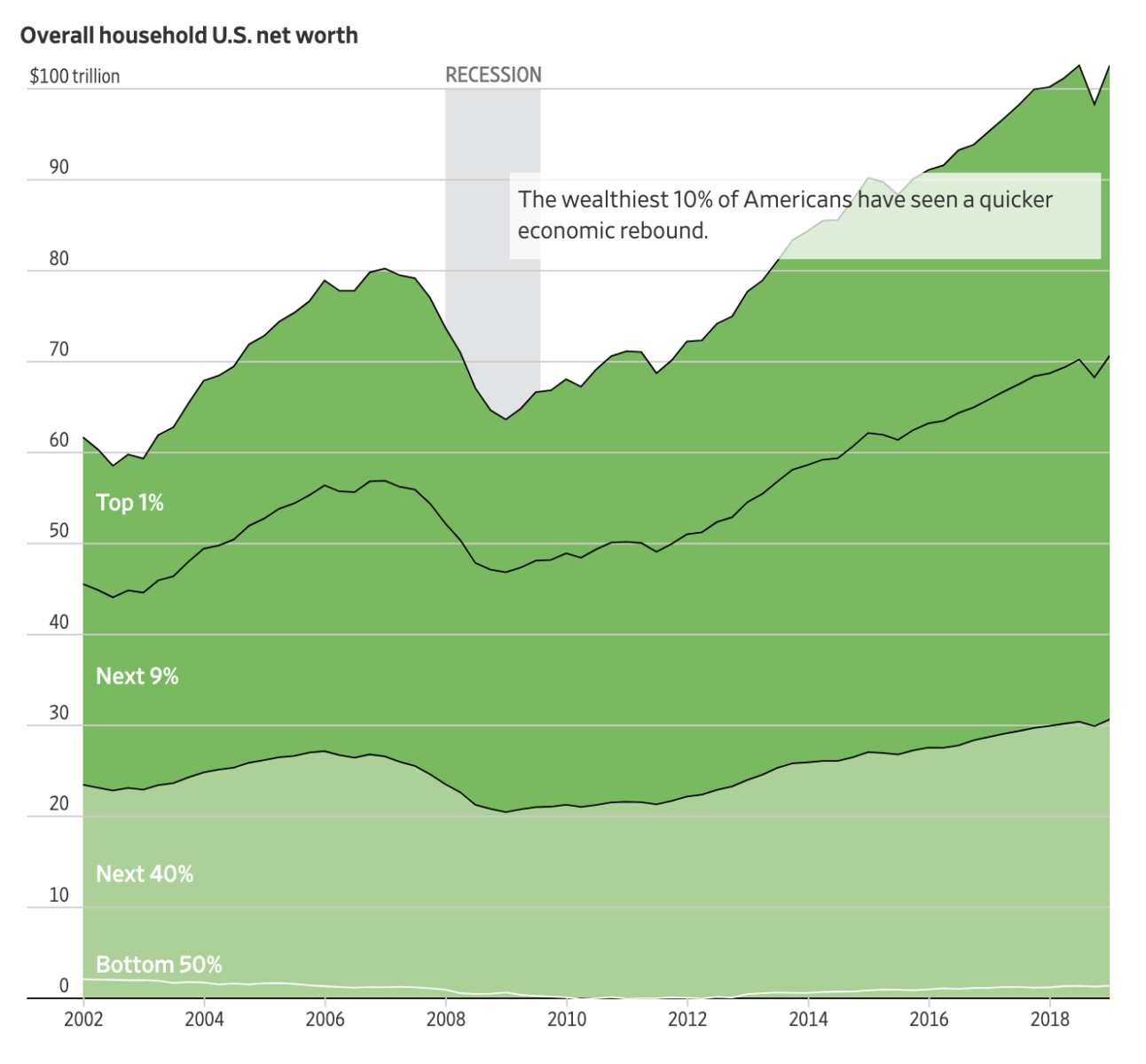

Source: Economic Policy Institute There is this weird counter-narrative to the wealth and income inequality issue. The data...

Source: Economic Policy Institute There is this weird counter-narrative to the wealth and income inequality issue. The data...

Source: Financial Times Today’s must read column comes from Martin Wolfe of the Financial Times: How to reform today’s...

Source: Financial Times Today’s must read column comes from Martin Wolfe of the Financial Times: How to reform today’s...

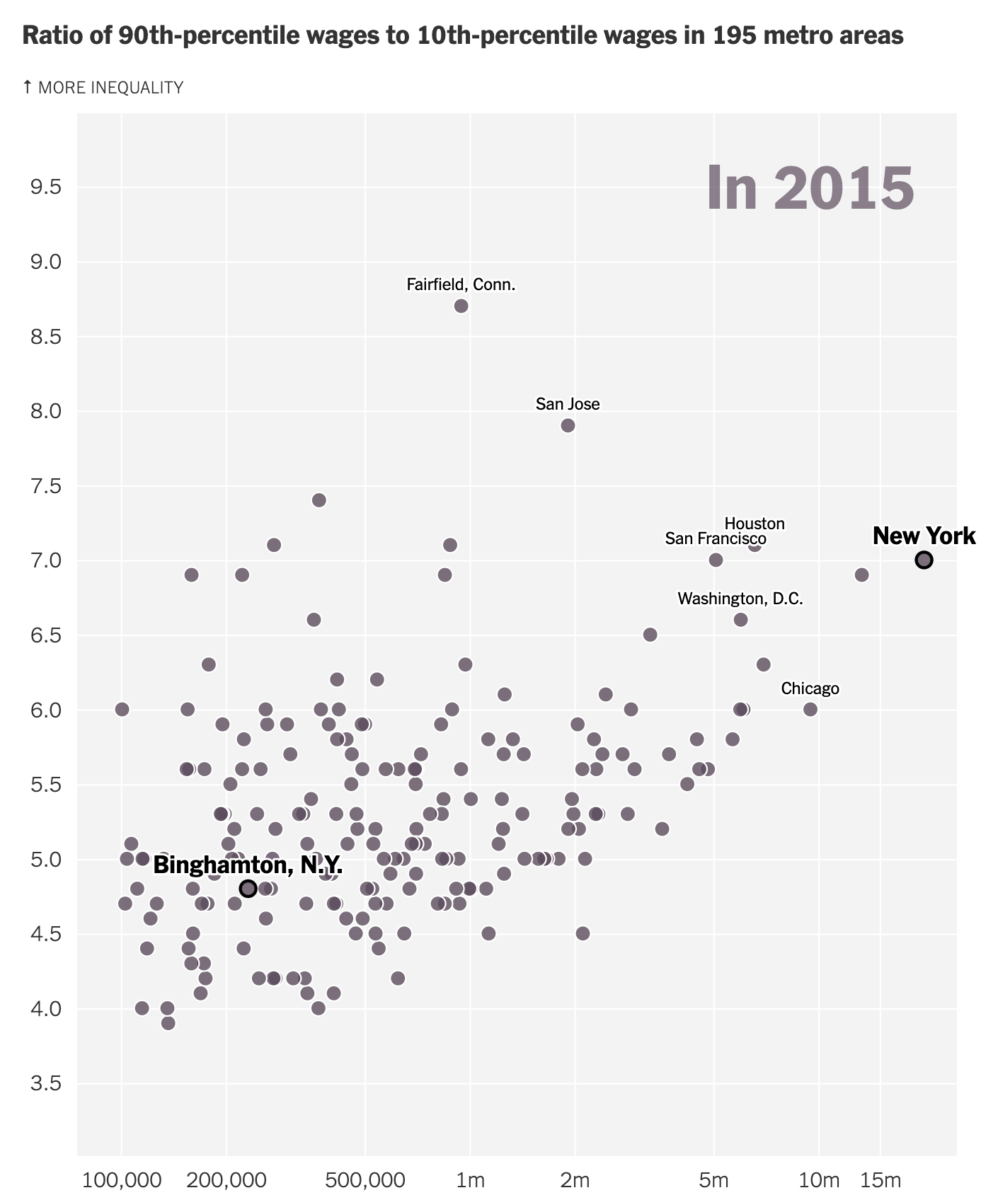

NYT: “Economic inequality has been rising everywhere in the United States. But it has been rising much more in the booming places...

NYT: “Economic inequality has been rising everywhere in the United States. But it has been rising much more in the booming places...

It’s Labor Day, when the Summer winds down, and we celebrate the American worker. Given the importance of Labor to the economy, it...

It’s Labor Day, when the Summer winds down, and we celebrate the American worker. Given the importance of Labor to the economy, it...

Get subscriber-only insights and news delivered by Barry every two weeks.