Head of World’s Largest Asset Manager: “Markets...

Washington’s Blog strives to provide real-time, well-researched and actionable information. George – the head writer at...

> Special IPO Edition! I will be on Power Lunch on CNBC at 1:30 pm debating the IPO market with Herb Greenberg, (whose take is here),...

> Special IPO Edition! I will be on Power Lunch on CNBC at 1:30 pm debating the IPO market with Herb Greenberg, (whose take is here),...

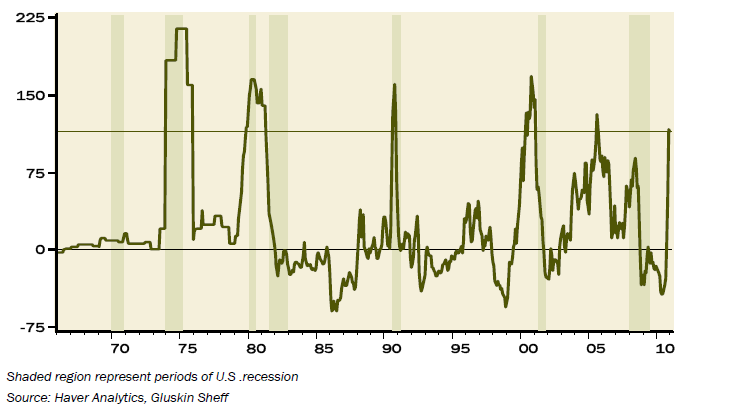

David Rosenberg of Gluskin Sheff calls the current doubling in the spot price of oil a “game changer: “There have been only...

David Rosenberg of Gluskin Sheff calls the current doubling in the spot price of oil a “game changer: “There have been only...

Get subscriber-only insights and news delivered by Barry every two weeks.