Examining the Consequences of Mortgage Irregularities for...

Please see attached report from the Congressional Oversight Panel. Examining the Consequences of Mortgage Irregularities for Financial...

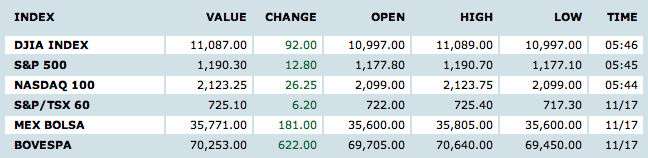

Futures screaming higher after the recent whackage on GM’s IPO and a and a European Union-led bailout package for Ireland (no word...

Futures screaming higher after the recent whackage on GM’s IPO and a and a European Union-led bailout package for Ireland (no word...

Awesome chart, from Dan Edstrom via Zero Hedge: > click for ginormous graphic

Awesome chart, from Dan Edstrom via Zero Hedge: > click for ginormous graphic

Get subscriber-only insights and news delivered by Barry every two weeks.