‘Should have paid the extra $2 an hour…’

Abelson on robo-signers last week: “Truth is, bankers just can’t stand prosperity, even after their near-death experience of...

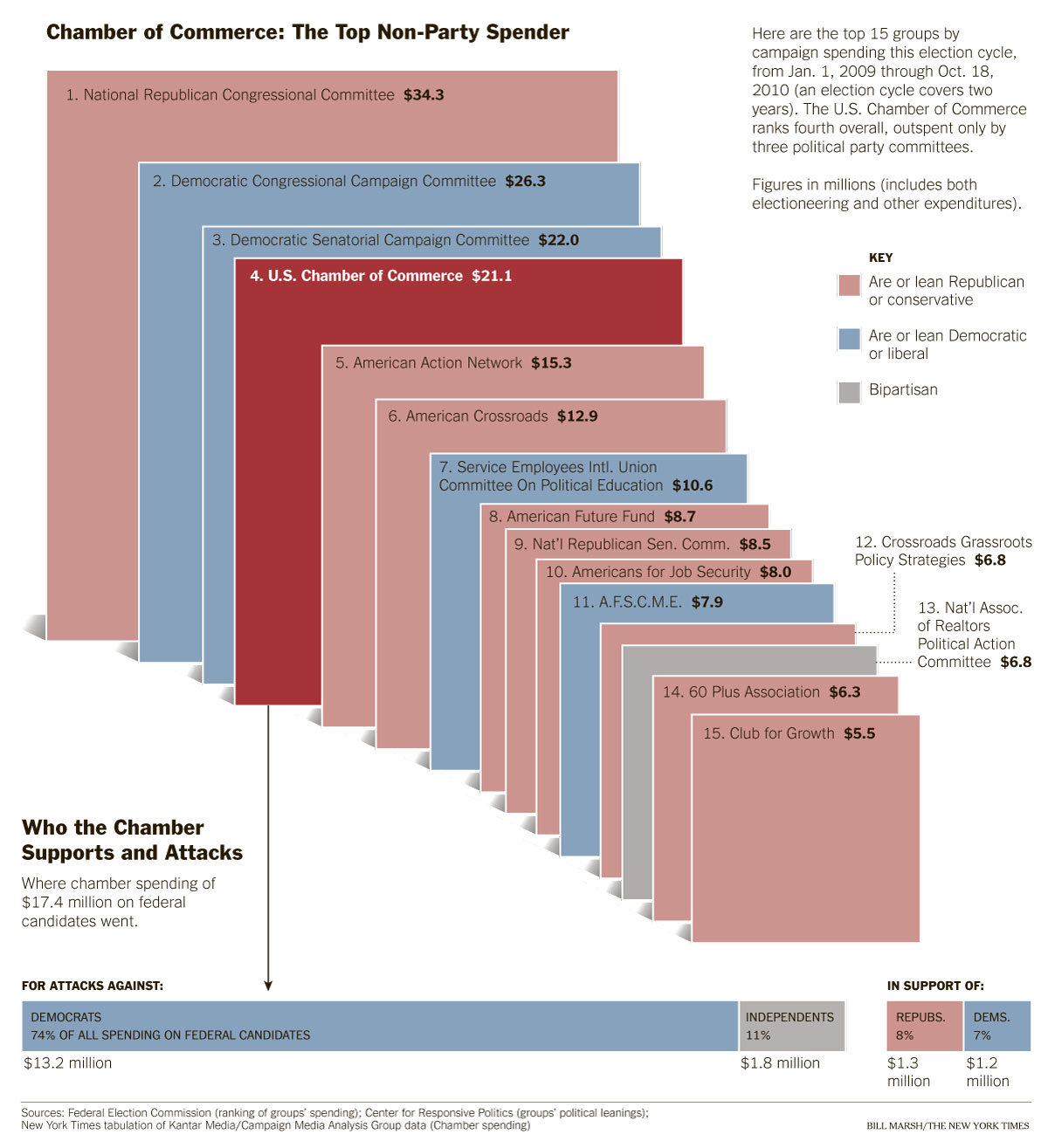

Fantastic chart, very consistent with my view that politics has been utterly corrupted by dirty corporate money. If you want to...

Fantastic chart, very consistent with my view that politics has been utterly corrupted by dirty corporate money. If you want to...

Get subscriber-only insights and news delivered by Barry every two weeks.