I am still modestly constructive on equities for the near term, but yesterday’s reversal was a potentially disturbing development....

Read More

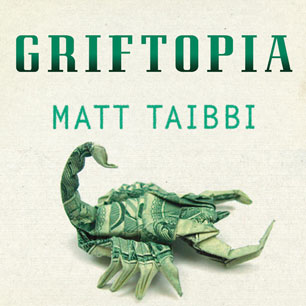

Matt Taibbi’s new book, Griftopia: Bubble Machines, Vampire Squids, and the Long Con That Is Breaking America, comes out next...

Matt Taibbi’s new book, Griftopia: Bubble Machines, Vampire Squids, and the Long Con That Is Breaking America, comes out next...

Read More

Ahead of the G20 meeting beginning today where currency rates will be the front and center discussion, the $ index is flattish. While...

Read More

Yes, its a parody (bajillionhits.biz) via Reformed Broker: > ~~~ Source: The Stephen Colbert of New Media by Ben Crair Daily Beast...

Read More

Christopher Whalen, managing director of Institutional Risk Analytics, talks with Bloomberg’s Mark Crumpton about the impact of...

Read More

These are the most interesting items I have come across on the current mayhem in the mortgage market. I do not expect this issue to pass...

Read More

Now that we seem to be past the talk of IF we’ll get another round of QE2 from the Fed, what’s left is HOW it will be...

Read More

~~~ Source: Are the Markets Prepared for Potential November Surprise Daniel Gross Yahoo Tech Ticker Oct 20, 2010...

Read More

I am digging this calendar from Jim Flora:

I am digging this calendar from Jim Flora:

Read More