Fiberglass Freaks’ have available for purchase officially licensed 1966 BATMOBILE Replica $150k. Is the car just a prop? Absolutely...

Fiberglass Freaks’ have available for purchase officially licensed 1966 BATMOBILE Replica $150k. Is the car just a prop? Absolutely...

Read More

Artist Anthony Freda, whose work has been featured here before, writes to say: Barry ‘ Love the left right post, you are indeed...

Artist Anthony Freda, whose work has been featured here before, writes to say: Barry ‘ Love the left right post, you are indeed...

Read More

With the QE, reflation trade back on today (buy gold, sell $’s, buy other commodities and currencies, buy Treasuries, buy stocks),...

Read More

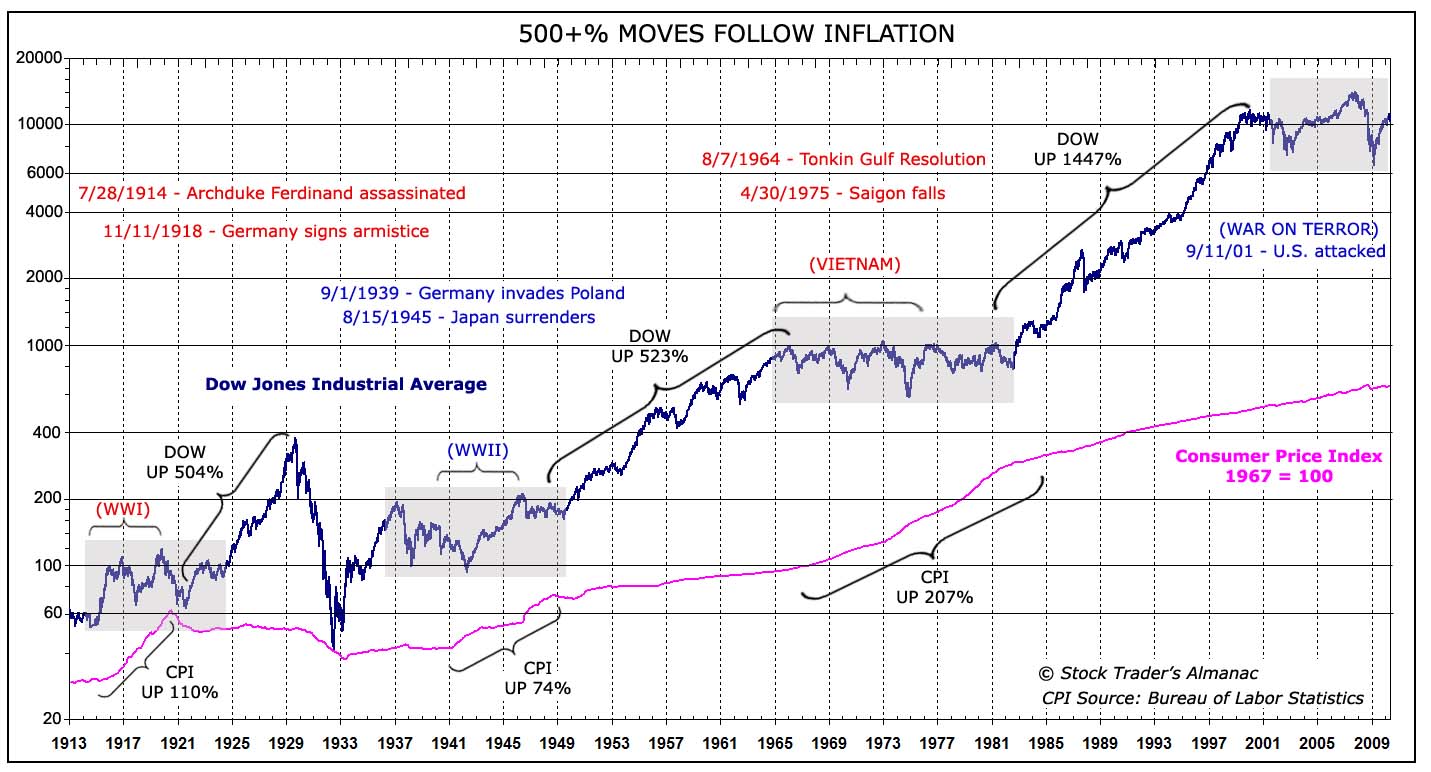

I mentioned this morning that Jeff Hirsch is the anti-Prechter — forecasting a wild $38K Dow in 2025. (Discussed this AM here, with...

I mentioned this morning that Jeff Hirsch is the anti-Prechter — forecasting a wild $38K Dow in 2025. (Discussed this AM here, with...

Read More

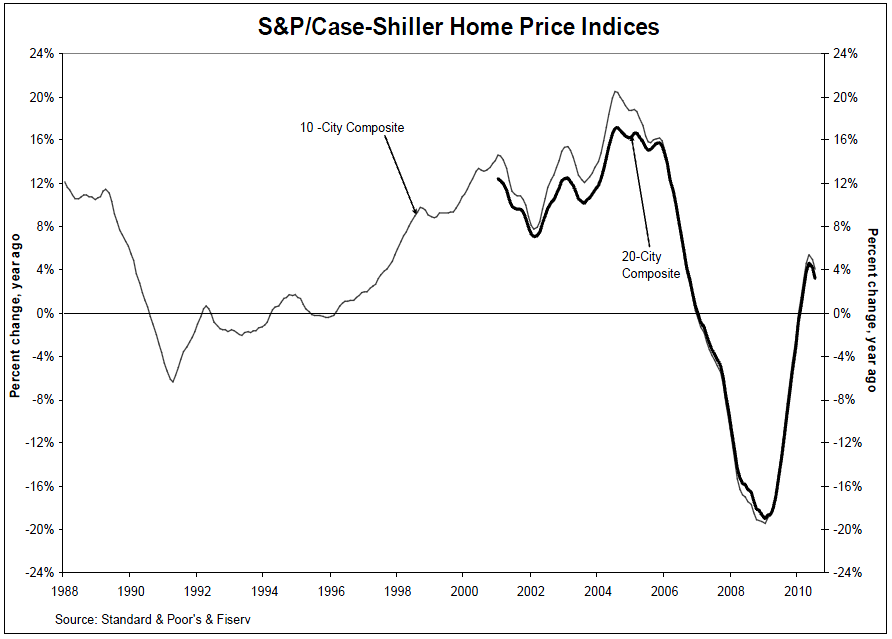

Case Shiller: “Home prices crept forward in July. Ten of the 20 cities saw year-over-year gains and only one – Las Vegas – made a...

Case Shiller: “Home prices crept forward in July. Ten of the 20 cities saw year-over-year gains and only one – Las Vegas – made a...

Read More

Next Super Boom — Dow 38820 By 2025 Stocks Catch Up With Inflation, But First Inflation Catches Up With Government Spending Jeffrey A....

Read More

The July S&P/CS 20 city home price index fell .13% m/o/m but was up 3.18% y/o/y, both about in line with expectations. The index at...

Read More

Ken Fisher channels my monkey comments to diss PIMCO’s Mohamed El-Erian and their “New Normal” thesis. I disagree with...

Read More

Soleil: Perspective Vince Farrell Soleil Securities Corporation Chief Investment Officer Phone: 212.380.4909 vfarrell-at-soleilgroup.com...

Read More

As the Fed continues to debate what form, if necessary, their next round of QE will take as evidenced by today’s WSJ article, the...

Read More