Last week, we reviewed the History of US Interest Rates: 1790-Present via Doug Kass. Following that, several of you pointed us to this...

Last week, we reviewed the History of US Interest Rates: 1790-Present via Doug Kass. Following that, several of you pointed us to this...

Read More

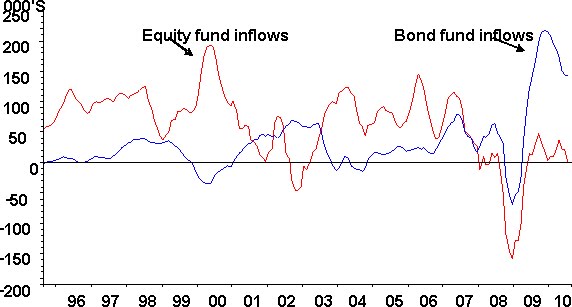

Much ink has been spilt over the question of whether government bonds are in a bubble or not. The bond bubble believers love to cite...

Much ink has been spilt over the question of whether government bonds are in a bubble or not. The bond bubble believers love to cite...

Read More

As we approach the 21st anniversary of the triumph of freedom and capitalism over oppression and central planning, I keep wondering if we...

Read More

“Lehman was forced into bankruptcy not because it neglected to act responsibly or seek solutions to the crisis, but because of a...

“Lehman was forced into bankruptcy not because it neglected to act responsibly or seek solutions to the crisis, but because of a...

Read More

Bull markets are born out of distress — witness March 2009. Bear Markets are born out of prosperity — witness 2008-early...

Read More

Retailers need a fresh start Andy Xie Caixin Online Aug. 30, 2010 > BEIJING: China’s gross domestic product surpassed Japan in...

Read More

FREAKONOMICS is the highly anticipated film version of the phenomenally bestselling book about incentives-based thinking by Steven Levitt...

Read More

What President Obama should do next for the economy, with Barry Ritholtz, FusionIQ. Wed. Sept. 1 2010 | :42:0 10 ET I need a hair cut!

Read More

> Tonite I will be on Fast Money on CNBC at 5:30pm discussing the next NFP, Tax Cuts, and big Infrastructure Stimulus. Temp tax cuts,...

> Tonite I will be on Fast Money on CNBC at 5:30pm discussing the next NFP, Tax Cuts, and big Infrastructure Stimulus. Temp tax cuts,...

Read More

I have recently been complaining about the excessive bearish sentiment. Whether it was Tony Robbin’s economic warnings, the...

I have recently been complaining about the excessive bearish sentiment. Whether it was Tony Robbin’s economic warnings, the...

Read More