Information is Beautiful has this tasty chartporn depicting the UK emergency budget: > click for larger graphic via The Guardian

Information is Beautiful has this tasty chartporn depicting the UK emergency budget: > click for larger graphic via The Guardian

Read More

This morning, we learned of a huge compromise in regulatory reform. The expectation was that no one was happy with the bill, but the...

Read More

5.0 out of 5 stars Great history lesson on government bailouts Great book on helping me understand how we got to the bailout mess we are...

5.0 out of 5 stars Great history lesson on government bailouts Great book on helping me understand how we got to the bailout mess we are...

Read More

I listened to Senator Bob Corker — and others — discuss the new financial regulations this morning. I was astonished to hear...

Read More

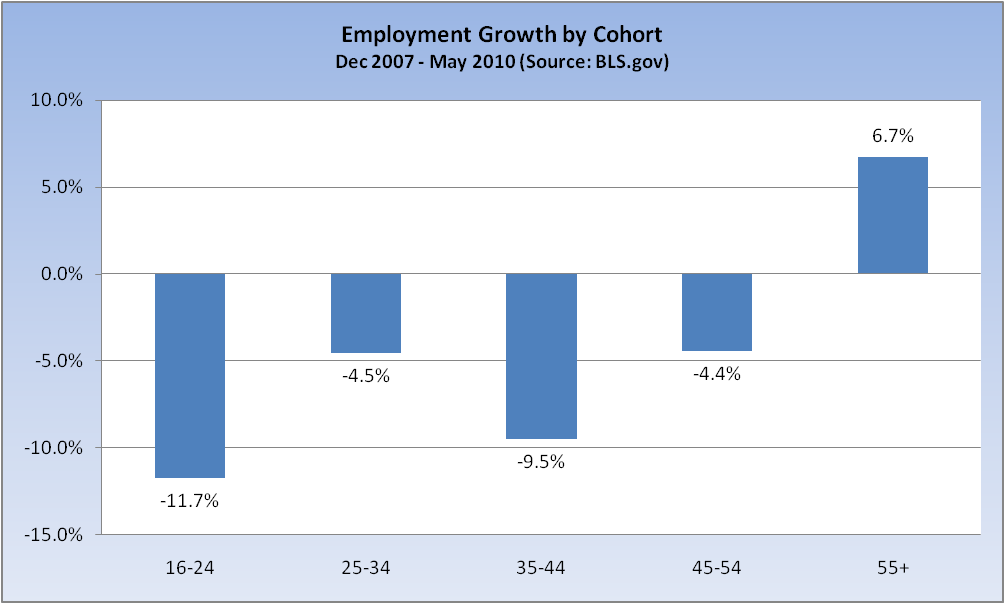

On a somewhat related note to my recent Kudlow post (that means it’s Invictus here, not BR, boys and girls), I see that in some...

On a somewhat related note to my recent Kudlow post (that means it’s Invictus here, not BR, boys and girls), I see that in some...

Read More

Of all days, TODAY ! Working on this . . . I listened to Senator Bob Corker — and others — discuss the new financial...

Read More

> Tonite I will be on Fast Money on CNBC for the full hour, discussing with the crew: – RIMM, Apple and iPhone 4.0 – BP...

> Tonite I will be on Fast Money on CNBC for the full hour, discussing with the crew: – RIMM, Apple and iPhone 4.0 – BP...

Read More

Dan Gross looks at why Fed Chair Ben Bernanke doesn’t seem too concerned about job losses.He disposes of the usual explanations,...

Read More